You finally found the perfect cotton twill. The hand feel is exactly what your brand needs. You negotiated the price down to a number that works for your margins. Then the invoice lands in your inbox, and the payment terms section reads "100% T/T before shipment." Your stomach knots up. You remember a colleague who wired $40,000 to a supplier in another country and waited six months for a container that never came. The fear of losing your capital to a stranger on the other side of the ocean is real. I hear this hesitation from almost every first-time buyer who contacts Shanghai Fumao. They love the fabric but they are terrified of the transaction.

We offer multiple secure payment structures specifically designed for U.S. cotton buyers, including Letter of Credit at Sight, SWIFT T/T with a balanced 30/70 split, and Alibaba Trade Assurance with credit card processing. We do not demand 100% upfront payment because that shifts the entire risk onto your shoulders. A fair partnership splits the risk. We structure our payment milestones to match our production milestones, so your money is always secured against tangible progress that you can verify before the next payment is released.

Payment should protect both sides of the table. I want to walk you through exactly how each method works in practice, the costs involved, and the paperwork you need to see before you release a single dollar. You will sleep better when you understand the safety nets built into these systems.

How Does A Letter Of Credit Work For Fabric Imports

A Letter of Credit is a contract written by banks, not by me or you. It is the safest payment method for a first-time buyer placing a large order over $50,000. Your bank, maybe Chase or Wells Fargo, issues an irrevocable promise to pay my bank, the Bank of China, the moment I hand over a perfectly clean set of shipping documents. I do not touch your money until I prove I loaded the right fabric onto the right ship on the right date. If I am one day late or the documents contain a single typo, the bank rejects the payment.

What Documents Does The Bank Check Before Release?

The bank does not care about fabric quality. They care about paper. Specifically, they check a stack of documents that must exactly match the terms written in the L/C. This stack typically includes the commercial invoice, the packing list, the marine bill of lading, the certificate of origin, and the inspection certificate.

The bill of lading is the trigger document. It proves the container physically left the port. The date on the bill of lading must be on or before the "latest shipment date" in the L/C. If the L/C says shipment by May 31st, and the bill of lading shows June 1st, the bank will refuse payment even if the delay was caused by a typhoon. This is why I always advise buyers to build a 7-day buffer into the latest shipment date. I also recommend adding a clause that allows the presentation of a third-party inspection report, such as an SGS or ITS certificate, as a mandatory document. This forces me to pay for an independent inspection before I can get your money. It protects you from the "box of rags" scam. For a complete checklist, you should review a detailed guide on required documents for a clean letter of credit presentation in cotton fabric imports. Missing one stamp can stall $100,000 for weeks.

How Much Does An L/C Cost For A Small Fabric Order?

L/Cs are secure but they are not free. Your issuing bank charges an opening fee, typically 0.5% to 1.5% of the L/C value, plus a flat documentation fee. My bank also charges an advising fee and a negotiation fee, which are usually deducted from the payment. On a $50,000 order, the total bank charges on both sides can easily reach $800 to $1,200.

This is why an L/C makes less sense for orders under $30,000. The fixed costs eat into the margin too aggressively. For smaller boutique brands doing an initial trial order of 500 yards, I usually steer them toward Trade Assurance or a simple T/T split because the bank fees are disproportionate to the transaction size. There is also the time factor. Setting up an L/C takes 5 to 7 banking days, and amendments cost money. If you change the color quantity after the L/C is issued, we have to amend the document, which is another $150 fee. However, for a bulk container order of 20,000 yards of cotton sateen, the security of an irrevocable L/C is worth every penny. Understanding the cost-benefit breakdown of using a letter of credit versus trade assurance for Chinese textile suppliers helps you make the right call for your specific cash flow situation.

What Is The Standard T/T Payment Structure For US Clients

Telegraphic Transfer, or T/T, is the workhorse of international trade. It is a direct bank wire from your account to ours. The risk with T/T is the trust gap. If you pay 100% upfront, you hold all the risk. If I ship 100% on credit, I hold all the risk. The solution is a staged payment schedule that aligns money with verified production progress.

Why Do We Use A 30% Deposit And 70% Before Shipment?

The 30/70 split is our standard because it mirrors our cash outlay. We spend approximately 30% of the order value on raw cotton yarn in the first week to begin warping and weaving your greige fabric. Your deposit funds that yarn purchase. You are not financing our factory overhead; you are financing the specific raw materials tagged to your purchase order.

The remaining 70% is due when the fabric is finished, inspected, and packed into cartons, ready to load into the container. Before you release that final payment, we send you a "Ready for Shipment" notification that includes photos of the packed rolls, the final inspection report from our QC team, and the label with the shipping mark. You verify that the goods exist and match your spec. Then you wire the balance. We load the container within 48 hours of receiving the funds. This way, your maximum exposure is 30% at any given time. That exposure is secured against the finished fabric sitting in our warehouse with your name on it. For more details on payment security, I recommend reading about industry standard T/T payment splits for importing textiles from China. The structure is designed to keep both parties honest through mutual dependency.

Can US Buyers Pay With A Credit Card Or PayPal?

Yes, for smaller orders and sample development. We process credit card payments and PayPal exclusively through our Alibaba Trade Assurance platform. This gives you a familiar checkout experience, and you get the fraud protection and chargeback rights that Visa or Mastercard provide.

However, credit card processing carries a significant merchant fee, typically 3.5% to 4.5% of the transaction value. For a $200 sample order, this fee is negligible. For a $30,000 bulk order, that fee is over $1,000. I am transparent about this cost. If you want the convenience and consumer protection of a credit card for a bulk payment, we can do it, but we add the processing fee to the invoice. Most buyers, once they trust our production process through a few small Trade Assurance orders, switch to T/T for the bulk business to save that fee. The smart path is usually: first sample order on Trade Assurance with Visa, first trial order of 500 yards on Trade Assurance, then bulk container order on T/T 30/70 with direct SWIFT transfer. This gradual escalation of trust protects you while minimizing transaction costs as the relationship deepens. It helps to check how to use Trade Assurance with a credit card for the initial small fabric order before transitioning to bank wire transfer.

How Does Alibaba Trade Assurance Protect My Cotton Order

Alibaba Trade Assurance is an escrow service. It is a virtual handshake enforced by a platform. You pay Alibaba, not me. Alibaba holds your money in a secure escrow account. I do not receive a single yuan until I provide a verified shipping tracking number and you confirm receipt of the goods within the agreed inspection window. If the fabric arrives late, or the quality does not match the online description, you file a dispute, and Alibaba's mediation team reviews the evidence and decides the outcome.

What Happens If The Fabric Quality Fails Inspection Under Trade Assurance?

You have leverage. The Trade Assurance contract specifies a quality standard, usually defined by our signed proforma invoice and the pre-production sample we both approved. When the container arrives at your warehouse, you have an agreed number of days, typically 15 to 30, to inspect the goods.

If you find a problem—for example, the fabric weight is 6oz instead of the 8oz we agreed upon, or the color is a visible mismatch—you take photos, you take a video, you cut a swatch and document the issue. Then you open a dispute on the Alibaba platform. Alibaba freezes the funds. Both sides upload evidence. If we are clearly at fault, I will authorize a refund for the defective portion or a negotiated discount. If we disagree on the severity, Alibaba's mediator reviews the case. The key to winning a dispute is having a clear, measurable specification in the original contract. "Blue" is subjective. "Pantone 19-4052 Classic Blue with a Delta E tolerance of less than 1.5" is objective and enforceable. I always help my buyers write technical specifications that a third-party mediator can verify with a spectrophotometer. Understanding the dispute resolution process for fabric quality claims on Trade Assurance for US buyers gives you a clear roadmap for protecting yourself.

Does Trade Assurance Cover Late Shipment Penalties?

Yes, and this is a feature I insist my new buyers use. The Trade Assurance order includes a "Dispatch Date" field. If I confirm that date and then miss it, the system can automatically trigger a penalty. The standard penalty is a percentage of the order value refunded to you for every day of delay, up to a capped amount.

I respect this penalty clause. It forces my production planning team to be realistic about lead times. I would rather quote you a 35-day lead time and deliver in 30 days than promise 25 days and trigger a late penalty. The penalty is not about the money; it is about discipline. It aligns my internal scheduling with my external promise. For a buyer, this is peace of mind. You can plan your cutting schedule around a guaranteed delivery date, knowing that if I slip, your holding costs are partially compensated. It transforms a vague promise into a contractual obligation with teeth. This platform-level enforcement is one reason I recommend small brands build their supply chain through verified suppliers who accept these terms. You can explore how Trade Assurance dispatch date penalties work for textile shipments from China to understand the exact compensation calculation.

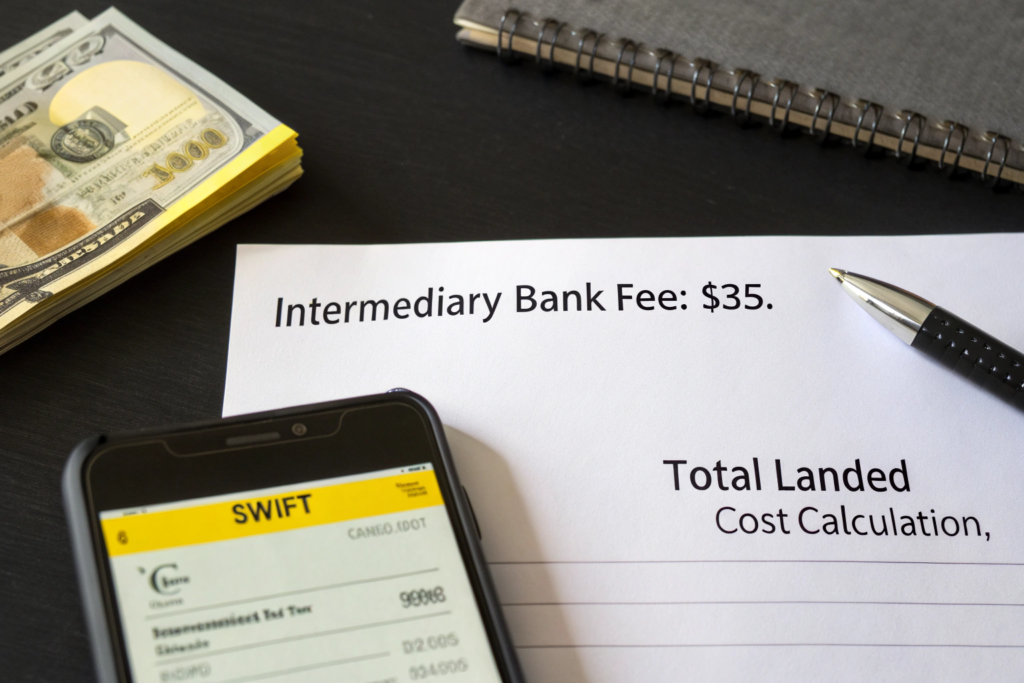

What Hidden Banking Fees Should US Buyers Expect

You wire $10,000 for a deposit. My bank receives $9,940. That missing $60 is not a fee I charged you. It is a fee skimmed by an intermediary correspondent bank somewhere between your regional bank in Ohio and my account in Zhejiang. These hidden banking fees are the silent margin killers in international trade. No one tells you about them until you check the bank statement and realize the numbers don't add up.

Why Do Intermediary Banks Take A Cut Of My Wire Transfer?

A SWIFT transfer does not travel directly from your small community bank to the Bank of China. It hops through one, sometimes two, large correspondent banks that act as clearing houses. Think of them as toll booths on the financial highway. JPMorgan Chase, Bank of New York Mellon, or HSBC typically sit in the middle of a US-to-China wire.

Each intermediary bank takes a flat fee, often $15 to $35, just for processing the transaction. This fee is deducted from the principal amount. If you are splitting a payment into a 30% deposit and a 70% balance, you pay this hidden toll twice. On a $10,000 deposit, a $35 fee is a minor annoyance. On a $100,000 order, the fees add up. The worst case is when a buyer sends the exact invoice amount and I receive short, which technically means the payment is incomplete and can delay the release of the shipping documents. I always instruct my U.S. clients to select the "OUR" instruction on the SWIFT form. This means the sender pays all banking charges, including intermediary fees. The amount I receive matches the invoice exactly. The fee is slightly higher upfront for you, but it eliminates the headache of a short-paid invoice holding up your container. For a clear explanation, you should look at how to instruct your US bank to send a SWIFT wire transfer with OUR charges for Chinese suppliers.

Are There Better Alternatives To Traditional Bank Wires?

Yes, fintech is slowly eating the old banking system. Services like Wise (formerly TransferWise) and Payoneer offer mid-market exchange rates with transparent, upfront fees that are often 50% to 80% lower than a traditional bank wire. The transfer speed is also faster, sometimes same-day.

However, these platforms have limits. Wise Business, for example, has a maximum transaction threshold that may not cover a $50,000 bulk fabric payment. They also operate differently. They do not use the SWIFT network; they have local bank accounts in each country and match the flows internally. This bypasses the intermediary bank toll booth entirely. For sample payments, development fees, and small trial orders under $5,000, I actively encourage my clients to use Wise. It saves everyone time and money. For large bulk production payments, the SWIFT system with the OUR instruction remains the most robust and auditable trail for our export tax rebate documentation. The payment landscape is shifting, and checking how to use fintech platforms like Wise or Payoneer to reduce wire transfer costs for importing fabric from Asia can save you hundreds of dollars per transaction. I want you to keep that money and spend it on better fabric.

Conclusion

Payment terms are the foundation of a sourcing relationship, not the fine print. A T/T 30/70 split protects your cash flow while funding the yarn on my spinning frame. A Letter of Credit wraps the transaction in bank-grade legal armor for your first container order. Alibaba Trade Assurance bridges the trust gap with an escrow service and a late shipment penalty that forces my factory to be honest about lead times. And understanding the hidden intermediary bank fees ensures the numbers in your spreadsheet match the numbers in my bank account. At Shanghai Fumao, I do not hide behind aggressive payment demands. I structure the transaction so that your money is always secured against verifiable production progress, whether that means a photo of your woven greige rolls, a third-party SGS inspection report, or a live video walkthrough of the packed cartons.

Stop letting payment anxiety block your access to premium cotton fabric. Let's start small to build the trust. Contact Elaine and ask her to set up a $200 sample order on Alibaba Trade Assurance with your credit card. Test our quality, test our communication, test the shipping speed. Once you are comfortable, we will structure the bulk payment terms that match your cash flow and your risk tolerance. Email elaine@fumaoclothing.com with your fabric requirements and your preferred payment method. Let's get your first invoice issued and your yarn spinning.