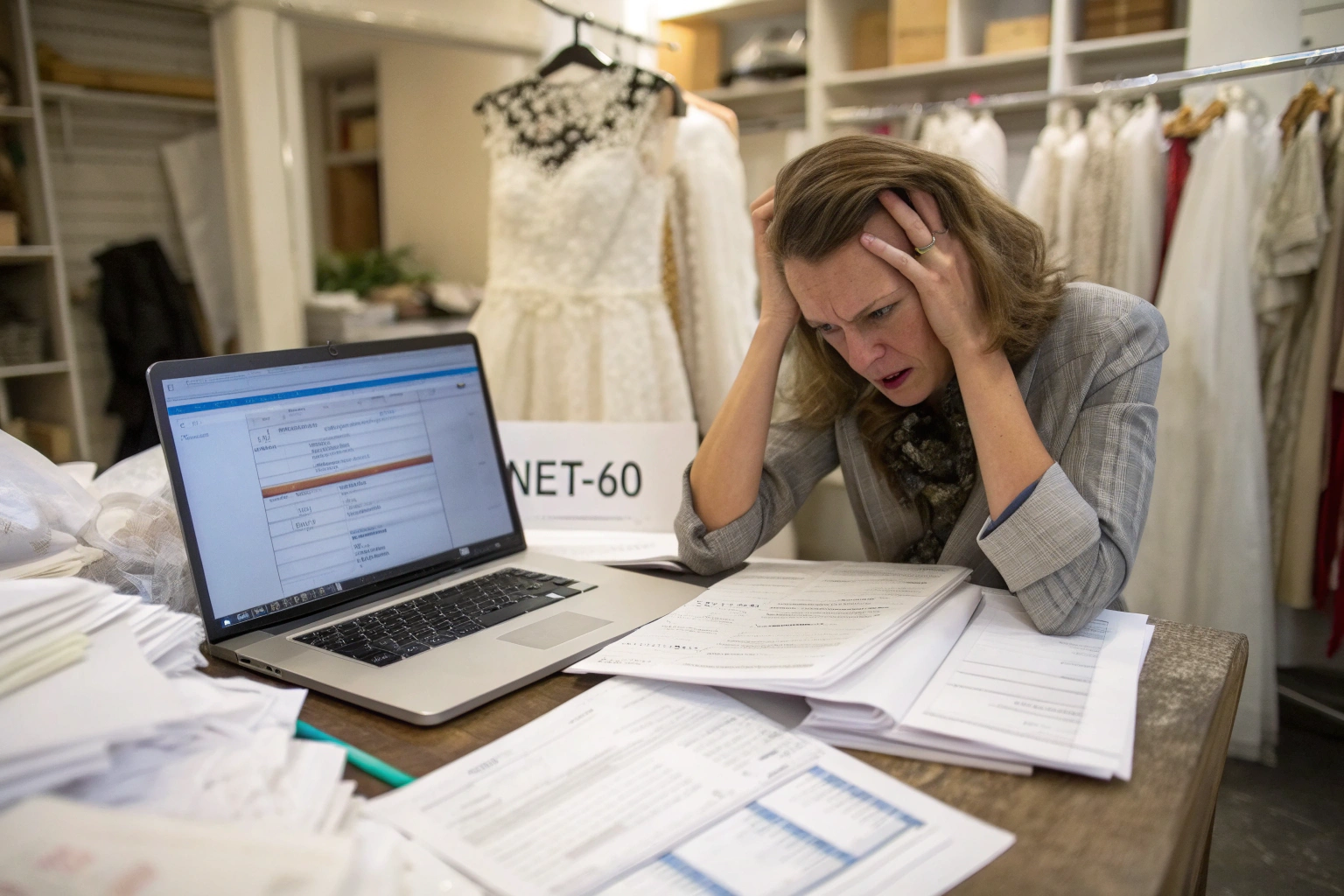

Cash flow is the silent killer of fashion brands, and you’re feeling the choke right now. You’ve got a buyer from a major department store who finally said “yes,” but their net-60 payment terms are staring at you like a loaded gun. Meanwhile, we’re asking for a 30% deposit to start your 5,000-meter custom cotton-linen blend, and the balance is due before the container leaves Shanghai. This “timing gap” is where dreams die. You’re not broke on paper—you’re profitable—but your money is trapped in inventory that hasn’t sold yet. The frustration isn’t the price per meter; it’s the suffocating pressure of bridging the 45 days between paying us and getting paid by your retailer. You’re essentially acting as an unlicensed bank, and the interest rates on your credit card are eating your margin alive.

You don’t need deeper pockets; you need smarter financial engineering that treats our fabric as a bankable asset. At Shanghai Fumao, we’ve structured deals for over two decades that turn our mill’s balance sheet into your working capital. The most direct route is our "staged production financing" model. Instead of one terrifying $50,000 wire transfer, we break your order into three payment milestones: a small sample-development deposit, a greige weaving release, and a final dyeing-and-finishing settlement. We physically warehouse your finished cotton-linen rolls in our Keqiao facility for up to 30 days at no charge, allowing your goods to sit "ex-works" while your retailer’s letter of credit matures. We can also connect you with third-party trade finance platforms we trust, who will pay us immediately on your behalf and give you 90-day open account terms, usually for a fee lower than a bank loan. This isn’t vendor financing; it’s using our 20-year stability to unlock liquidity you didn’t know you had.

Look, I remember a time back in 2018 when a client from Melbourne was panicking over a large order of our bamboo-linen sheeting. They had the sales, but the bank saw a "risky import business." We sat down, restructured the delivery into three phased shipments, and aligned the payments with their trade show deposit inflows. That’s the kind of granular problem-solving we bring. In this article, I’ll walk you through the exact mechanisms we use—from letters of credit to purchase order funding—so you can stop stressing about the wiring deadline and start focusing on selling that beautiful cotton-linen at full margin. Stick with me; this might just save your next big break.

What Are the Best Payment Terms for Bulk Fabric Orders?

You’ve probably been burned by a supplier who treats your cash like an interest-free loan. The standard "30% deposit, 70% before shipment" can feel like a hostage situation. Your money is gone, the goods aren’t here, and if the quality is off, you have zero leverage. This "pre-shipment anxiety" is brutal. You’re staring at a blank wire confirmation screen, knowing you’re about to lose all your bargaining power the second you hit send. The problem isn’t the deposit itself; it’s the massive information asymmetry that favors the supplier over the buyer.

The key to safe payment terms is decoupling the "production risk" from the "quality risk." The deposit should only cover raw materials, not your trust. We address this by offering a Letter of Credit (L/C) at sight for orders over $50,000. This is the gold standard for international trade. Your bank guarantees our payment, but only after we present a strict set of documents—including a SGS or ITS third-party inspection certificate. This flips the script. Instead of you trusting our word that the cotton-linen blend is 55/45, the bank verifies it against the certificate. We also accommodate Documentary Collections (D/P) for mid-range orders, which is cheaper than an L/C but still keeps the title documents with your bank until payment. It’s not about distrust; it’s about building a paper fortress that protects both sides from the chaos of global shipping.

But here’s what most suppliers won’t tell you: the most valuable "term" isn't the payment method; it's the payment schedule. We often tie milestones to specific production photos from our factory floor. For a large cotton-linen run, we ask for a deposit to secure the loom, a second payment when we send a video of the greige fabric rolling off the rapier machines, and the final balance against the faxed copy of the bill of lading. This keeps you in the loop and keeps your cash flow synchronized with our actual output. (Let me drop a quick insider tip: avoid suppliers who demand 100% upfront for "custom" blends. A 50/50 cotton-linen is standard; they shouldn't need all your cash to start.)

How Does a Letter of Credit Protect My Cotton Linen Order?

An L/C isn't just a payment method; it’s a contractual firewall. You fear that the shirting fabric will arrive with streaks or inconsistent slubs. With an L/C, you can specify that we must present an "Inspection Certificate" signed by a specific, agreed-upon inspection agency. If our cotton-linen fails the 4-point grading system, the inspector won’t sign. If the inspector doesn’t sign, our bank doesn’t get paid. It's binary; we pass, or we don't get the wire.

We negotiate these terms clearly upfront. You write the credit to require a detailed report showing the average yarn count and the shrinkage test result. We’ve shipped to U.S. clients who require an "AATCC 135 shrinkage result below 2%" written directly into the L/C text. It forces our quality control team to be meticulous because a single loose thread on a lab report can cause a "discrepancy," delaying our payment by weeks. This bank-enforced accountability is much stronger than any email promise. It essentially transfers the final quality inspection from a subjective "looks good" to an objective, legally binding checklist.

Can I Negotiate Deferred Payment Using Trade Finance Platforms?

Banks are slow. They want three years of audited financials, your firstborn, and a blood test. If you’re growing fast and don’t have pristine books, you need an alternative. New digital trade platforms are filling this gap. They effectively act as a "buy now, pay later" for B2B textile imports. Instead of scrutinizing your whole business history, they underwrite the transaction. They look at the purchase order from your end buyer and the track record of the supplier—that’s us.

We’ve integrated with several of these fintech lenders who can approve a credit line of up to $200,000 in 48 hours. You place the order with Shanghai Fumao for your cotton-linen romper fabric, the platform pays us upfront at the 30% deposit milestone, and then they pay us the balance when we are ready to ship. You repay the platform over 60 or 90 days. Yes, there’s a discount fee, usually 2-3% of the invoice value. But think about it: if financing 10,000 meters of fabric at 3% saves you from losing a $100,000 wholesale contract, that’s a 30x return on the cost of capital. It converts a cash-flow crisis into a manageable line item.

How to Unlock Working Capital Trapped in Inventory?

You’re "asset-rich" but "cash-poor," and that’s a terrifying place to be. Your warehouse has shelves full of beautiful cotton-linen fabric, but your bank account is empty. You’ve already paid the duty, the freight, and the production cost, and the money is just sitting there in cardboard boxes. This inventory trap is the most common reason growing brands fail. They don't go bust because they lack orders; they go bust because they miscalculated the velocity of their cash. The fabric isn't money until it’s a garment with a tag on it, and right now, it’s just a very expensive pile of potential.

The trick is to borrow against the value of the finished fabric, not your personal credit score. At Shanghai Fumao, we help our clients unlock this trapped capital by extending our warehousing and just-in-time delivery model. Instead of shipping the entire 8,000 meters of your cotton-linen trouser fabric in one go, we hold it in our Keqiao bonded warehouse. You draw down inventory in monthly installments of 2,000 meters. This means your duty and freight payments are staggered over four months, perfectly aligning with your retail sales season. You turn a massive upfront cash drain into a monthly operating expense, freeing up your existing cash to fund marketing or new samples. It’s a very simple concept: we store the bulk, you pay for the flow.

Beyond physical warehousing, you can use the ownership of the goods to get a loan. Since our cotton-linen is a standard, non-perishable commodity with a clear market value, specialized inventory lenders will accept it as collateral. We issue a "warehouse receipt" that certifies the exact specification, quantity, and storage location of your fabric. You take this receipt to an asset-based lender. Because the fabric is stored in our secure, climate-controlled facility—and because we can provide a formal valuation of the greige stock—the lender can advance you up to 50% of the fabric’s market value. It keeps your business liquid while you wait for your customers to pay their invoices, effectively turning our factory into your private bank vault.

How Does Just-in-Time Delivery Reduce Upfront Cash Burden?

Holding inventory is expensive. A container of cotton-linen sits in your local warehouse, costing you rent, insurance, and the mental weight of "I need to sell this now." Just-in-Time (JIT) delivery from our factory eliminates these holding costs entirely. You don't pay for storage you don't need. Instead, you integrate our shipping schedule with your production calendar.

For a client making seasonal resort wear in California, we do this precisely. They forecast a need for 3,000 meters of printed cotton-linen per month. We weave and finish the bulk in one go to get the cost down, but we only charge them for the warehousing logistics, which is a fraction of the U.S. domestic storage fee. We ship exactly 3,000 meters on the 1st of the month. Their cash outlay is smooth and predictable, not a scary spike. This method also mitigates the risk of a trend dying. If the season is a flop, they can adjust the dye or print for the next batch before we cut the rest, something impossible if they’d imported the whole lot at once.

What Is Purchase Order Financing and How Does It Work?

What if the order is so large that even the 30% deposit is out of reach? You need the money before you pay us. This is where Purchase Order (P.O.) financing comes in. It sounds like a miracle, and frankly, for a brand with a solid sales contract, it is. A P.O. financing company advances you the capital specifically to pay your supplier to produce goods that have already been sold.

Here’s the real-world flow: you secure an order from a boutique chain for 1,000 units of a cotton-linen blazer. You send the P.O. to a financing firm and get an approval to fund the transaction. They issue a letter of credit or direct payment to Shanghai Fumao. We produce the fabric and the goods, ship them, and the retailer eventually pays the financer directly, minus their fees. It’s a closed-loop system. The lender’s security isn't your balance sheet; it’s the creditworthiness of your customer. We support this process by providing transparent production timelines and weekly status photos, giving the P.O. lender the confidence that we will deliver on time, which triggers their funding release.

How to Mitigate Currency Risk When Buying Asian Textiles?

You quote your collection in U.S. dollars, but we quote our cotton-linen in USD too. Seems simple, right? Wrong. The moment the Federal Reserve sneezes and the Chinese Yuan strengthens against the dollar, our local costs rise. If we re-price this volatility into your next order, your margin evaporates overnight. You’re not a currency trader, but a 5% swing in the exchange rate can wipe out a 10% net profit margin on a large textile order. The anxiety hits when you realize you’re exposed to a macro-economic war between two central banks, and all you wanted was to buy some really nice linen for a summer dress.

The simplest hedge is to lock in the price in your contract for a fixed window. At Shanghai Fumao, we offer a "price validity period" of 30 to 60 days on all our cotton-linen quotes. This gives you a risk-free window to finalize your own selling prices. For longer-term projects, we share the risk. If you’re working on a 6-month development cycle, we can structure a "currency collar" agreement. We set a floor and a ceiling on the exchange rate band. If the USD/CNY rate fluctuates within that band, the price stays fixed. If it breaks out of the band, we split the difference. This prevents a shock for either side. We also allow clients to pay in multiple tranches using a Forward Contract through their bank, locking in today’s rate for a payment that happens in June 2025. It costs a small deposit, but it’s insurance against a potential tariff or currency spike.

But transparency is the ultimate risk mitigation. We don't hide a "buffer" in our price to protect ourselves; we break the cost down. We show you the raw material cost of the cotton and flax, the labor, and the processing, all in RMB. Then we apply the current exchange rate. When the rate moves, you see exactly why the price adjusted, which builds trust rather than suspicion. (This is crucial: many importers get ripped off by suppliers who pocket the currency gains and pass on the losses. We don't play that game.)

![]()

Should I Pay in RMB or USD for Large Fabric Orders?

This is the million-dollar question. Most American buyers instinctively default to USD because it feels safer. But paying in RMB can sometimes save you serious money, especially if you hold RMB in an offshore account or if you source from multiple Chinese vendors.

If you pay in USD, we take the exchange risk, so we will naturally build a small margin of safety into the conversion. If you pay directly in RMB, you take the exchange risk, but you can control the timing of the conversion. You wait for a favorable dollar-strength day and wire the money. For a recent shipment of 8,000 meters of cotton-linen canvas to Texas, we quoted a client both ways. By paying in RMB through a Wise business account, they saved about 1.8% compared to our USD wire price, simply because they converted on a day with a lower mid-market rate. It requires more financial sophistication, but on a $60,000 order, a 1.8% saving is over a thousand bucks—real money that goes straight to the bottom line.

How Do Forward Contracts Protect My Fabric Budget?

A forward contract lets you sleep at night. You decide your budget six months in advance, and you need to know the fabric won't blow that budget. A forward contract with your bank freezes the exchange rate. You agree to buy a specific amount of USD against RMB on a specific future date. When our invoice comes due in three months, you buy the RMB at the old rate.

This is how large corporations operate, and it’s accessible to small businesses too. It removes the "speculation tax." Let’s say you have a $40,000 order for our eco-friendly cotton-linen. You lock the rate at 7.2 RMB to the dollar. If the rate falls to 6.9 by the time we ship, you’ve just saved thousands because you’re still buying at 7.2. You pay a deposit for this privilege, but it’s a known cost. We help by providing exact invoice dates early so your bank can set the maturity date precisely. It transforms a variable gamble into a fixed cost, letting you price your wholesale clothing accurately and protect your brand’s gross margin.

How to Build Long-Term Credit with a Chinese Textile Mill?

The first order with a new supplier is always a cold, hard cash transaction. You feel like a stranger, and we treat you cautiously because we’ve been burned by chargebacks before. But you want to graduate from "cash against documents" to "open account" terms where you pay 30 days after receiving the goods. This is the ultimate goal—it mirrors the domestic buying experience, but it requires trust that usually takes years to build. The pain is the waiting; you know you’re good for the money, but we don't know it yet, and that lack of history is keeping your cash flow tied up.

Building trade credit with us is like building a personal relationship; it accelerates with reliability and transparency. The fastest way to earn credit terms is to consistently nail your specifications and avoid last-minute order changes that cause us downtime. We track your "order stability index" internally. If you order 3,000 meters of the same unbleached cotton-linen three times in a year, with clean technical packs, you’re a dream client. We start by offering a retroactive discount on the third order, and by the fourth, we might offer a net-30 account on a small trial volume. At Shanghai Fumao, we also boost your "trust score" when you actively use our QR code tracking system. When we see you logging in to check the inspection data, we know you are a serious professional, not a fly-by-night speculator. This engagement signals that you understand the product, reducing our perceived risk.

Remember, a fabric mill isn't a bank, but we want to finance our best clients to keep them coming back. We are much more likely to extend credit to a brand that has visited our Keqiao facility or done a video walkthrough. It makes the relationship human. For a client in London who had been with us since 2021, we started offering split payments—50% upfront, 50% 60 days after bill of lading—after she consistently showed us that her sell-through rate was high. She effectively proved that our fabric moved fast, meaning her business was healthy. We didn't look at her balance sheet; we looked at her order frequency and consistency. That’s a credit model built on mutual success, not just FICO scores.

What Does It Take to Graduate from Proforma to Open Account?

It’s a leap of faith for us to ship a container without the balance payment. To get there, you need to provide a "credit narrative," not just a bank statement. Proforma invoices are the dating phase. Open accounts are the marriage. We need to see stability in your brand, such as a consistent purchase history over at least 12 months, ideally spanning two of our busy production cycles like the March-to-May window and the autumn rush.

We also look at your communication discipline. If you confirm the lab dip in 24 hours and sign off the shipping sample without endless debate, you’re signaling that you respect our turnaround time. This efficiency matters. A quick decision-maker saves us money, so we reward that with flexible terms. We will often ask for a "guarantee" in the form of a post-dated check or a personal guarantee from the director for the first open-account transaction. It’s a symbolic safety net. Once that first net-60 transaction clears smoothly, the guarantee is torn up, and you’ve officially transitioned from a risky new buyer to a trusted partner.

How Can Repeated Small Orders Lead to Bigger Financing Flexibility?

Don’t underestimate the strategic power of a small, boring order. A perfectly executed 500-meter order of plain cotton-linen voile is worth more to our credit team than a chaotic 5,000-meter order. Small orders let you build a "credit history" at a low cost. You prove you can handle the logistics, the customs clearance, and the payment without drama.

Think of it as a proof of concept for your business hygiene. If you routinely buy small batches and wire the payment within 24 hours of the invoice, we notice. We start to flag your account as "low maintenance." This status is gold. When you finally need a massive $80,000 line for a sudden cotton-linen bomber jacket trend, we are willing to negotiate terms that we’d never offer a new, untested buyer. We might even help co-finance the raw cotton procurement if you share the purchase order from your end customer. You’ve trained us through a series of small wins, like reps in a gym, building the muscle memory of trust that allows us to confidently say "yes" to your big ask.

Conclusion

Financing a large cotton-linen purchase shouldn't feel like a high-wire act without a safety net. We’ve unpacked the entire toolkit, from using rock-solid Letters of Credit and digital trade finance platforms to bridge the timing gap, to leveraging our Keqiao warehouse as a storage facility that defers your shipping costs. We’ve seen that inventory doesn’t have to be a cash trap—it can be collateral—and that Purchase Order funding can essentially turn a retailer's credit card into your production budget. Smart currency hedging, whether it’s a simple forward contract or paying in RMB, ensures that a politician’s speech doesn’t wipe out your fabric margin overnight.

The ultimate goal, however, is to transcend these financial instruments altogether. The most cost-effective financing isn't a loan; it’s a long-term partnership with a mill that trusts you. By starting small, communicating clearly, and proving your sell-through speed, you earn the ultimate prize: open account terms that turn our textile mill into an extension of your cash flow cycle. Real profitability in this industry doesn’t come from squeezing the price per meter down by ten cents; it comes from synchronizing the rhythm of your payments with the rhythm of your sales.

If you’re sitting on a large purchase order and feel stuck, don’t let cash paralysis kill the deal. We sit right in the heart of the Keqiao textile cluster, and we’ve seen every financial trick in the book, from the standard to the highly creative. Let’s look at your specific cotton-linen project and design a financing roadmap that works for your actual sales cycle, not against it. At Shanghai Fumao, we’re committed to acting as your growth partner, not just a supplier. For a confidential discussion on how to structure your next big payment and secure your supply chain, reach out directly to our Business Director, Elaine. She’s handled these negotiations for decades. Email her your situation at elaine@fumaoclothing.com. Let’s turn that scary invoice into your biggest profit win.