Let me tell you what keeps a textile mill owner awake at 3 AM. It is not a loom breakdown. It is not a dye lot variation. It is a 40,000-meter custom order of Italian-grade wool blend sitting in our warehouse, fully finished, perfectly inspected, and the buyer has gone silent. I have been in this business for twenty years, and I have seen brilliant fabric collections die on the shelf because the payment structure was a gentleman’s handshake built on hope. Custom high-end fabric is not a commodity. You cannot just resell a batch of specially engineered Japanese-vibe crinkled chiffon to the next guy if the original buyer walks away. That fabric is uniquely yours—the color you matched, the hand feel you approved, the width you specified. That is why payment terms in this industry are not just administrative formalities. They are the financial architecture that either protects or destroys a partnership. Get them wrong, and you are not just out the fabric cost; you are out the raw material, the labor, the machine time, and the opportunity cost of a loom that could have been running a safer order.

The standard payment structure for custom high-end fabric development with a reputable Chinese manufacturer like Shanghai Fumao is not a mystery, but it is also not negotiable down to zero risk for the buyer. It typically involves a 30% to 50% deposit to initiate the order, with the balance paid before shipment. This is not greed. This is physics. When we accept your custom order, we immediately commit cash to purchase specific raw yarns. If your design requires a rare 120s mercerized Egyptian cotton or a GRS-certified recycled polyester filament, we cannot just pull that from general stock. We order it specifically for you. The deposit covers that raw material risk. The balance before shipment is the final gate—it ensures that when that container leaves Ningbo port, both parties have skin in the game. You have paid for goods you inspected via digital photos or third-party QC reports, and we have produced goods that meet the spec. I had a client in 2023, a luxury streetwear brand from Los Angeles, who tried to negotiate 100% payment after delivery on a custom jacquard denim project. I had to respectfully decline. The yarn alone cost us $28,000 to import. That is not a credit line we can extend while a container floats across the Pacific for 30 days.

But here is what I want to emphasize: payment terms are not just about the percentage split; they are about milestones, trust signals, and your ability to secure a production slot in a busy factory. The terms you agree on will dictate how fast your sampling moves and how seriously your order is treated among a sea of competing orders. Now, I will walk you through the exact financial flows, the hidden fees that trap inexperienced buyers, and the negotiation levers you actually can pull to protect your cash without insulting the factory’s risk management. At Shanghai Fumao, we have refined our payment architecture to work for both one-man startup designers and multinational retailers, and I will show you exactly how that structure works and why.

What Is the Standard Deposit and Balance Structure for Custom Textile Orders?

The classic formula in the textile industry is 30/70, but for high-end custom work, I often tell my clients at Shanghai Fumao to expect a 50/50 split. Let me break that down so there is zero confusion. A 30% deposit means you pay 30% of the total invoice value when you sign the proforma invoice. We then order the yarn and schedule the looming. The remaining 70% is due when the fabric is finished, inspected, and packed—before the container doors close. A 50% deposit usually applies when the order is either highly specialized with zero resale value, or when the raw material cost is exceptionally high. A pure silk charmeuse custom dyed to a specific Pantone shade, for example, will likely require a 50% deposit because if you cancel, we are holding a color that only works for your bridal collection. The logic is not punitive; it is actuarial.

I remember a specific negotiation in early 2024 with an Australian formalwear brand. They wanted 1,500 meters of a custom-developed bamboo silk blend in a proprietary teal. Our raw bamboo silk greige cost was significant. They pushed for 20/80 terms, citing their company’s long history. I counter-offered with a milestone-based 40/30/30 structure: 40% to commit raw materials, 30% upon sample approval and bulk weaving start, and 30% before shipment. This structure actually gave them more control because the second payment was tied to a visible milestone—they saw the approved sample and the first 100 meters of loom-state fabric before releasing the second tranche. That middle milestone is a powerful trust builder. It says, "We are confident enough to start production before full cash is in hand, but we need to share the risk at each phase." You should always ask for a milestone-based payment schedule if the 50% deposit frightens your CFO. It breaks the risk into digestible chunks.

Why Do Custom Fabric Orders Require Higher Upfront Deposits Than Stock Fabrics?

The answer lies in the concept of "fashion risk." A stock fabric, like a basic black polyester lining, has universal demand. If you cancel a stock order, we can sell that black lining to the next client next week. The inventory converts to cash quickly. A custom fabric is the opposite of liquid. It is an illiquid asset. That teal bamboo silk I mentioned earlier? If the Australian brand cancels, I cannot just sell it to a random US buyer. The US buyer might want a slightly different teal, or they might need 300 meters and I am stuck with 1,200 meters of deadstock. The deposit compensates us for that illiquidity. It also covers the "sampling amortization." On a custom order, you are not paying a $500 development fee per se. You are paying for the bulk fabric, and we often absorb the sampling cost into the bulk margin. But if you walk away after we have spent $1,200 in dyestuffs and lab time perfecting your custom color, the deposit ensures we are not paying for your R&D out of our own pocket.

I want to give you a real technical example of why raw materials are so sensitive. Suppose your custom fabric involves a fine merino wool blended with Tencel. The merino wool price fluctuates weekly based on Australian auction markets. We lock in your yarn price the day we receive the deposit. If you delay the deposit by two weeks and the wool auction price jumps 8%, we either have to absorb that loss or re-negotiate the price with you. Neither is good for the relationship. The deposit is effectively a hedging instrument. It allows us to buy the raw material futures at the moment of commitment. I had a bitter lesson in 2015 when I trusted a long-term client with a yarn order without a deposit. The wool price spiked due to a supply drought, and we lost $4,000 on a small batch. From that day on, I made it a rigid rule: no deposit, no yarn order. Period. The deposit protects the mill from commodity volatility.

Is It Possible to Negotiate Lower Deposits for Long-Term Reorder Partnerships?

Yes, absolutely, and this is where loyalty pays dividends. After you have completed three or four successful, on-time, zero-dispute orders with Shanghai Fumao, I consider you a strategic partner. At that stage, the trust is no longer theoretical; it is documented in the shipped containers and the clean QC reports. For these partners, I am willing to negotiate a reduced deposit structure, sometimes as low as 20% or even 15% for repeat orders of the same custom quality. The logic is that your custom quality is no longer "custom" to us; it is now part of our internal stock-keeping system. We have the dye recipe registered in our spectro database under your brand code. We know your quality tolerances. The raw yarn lead time is predictable. The risk of cancellation is significantly lower because your brand depends on that supply chain continuity. A London-based bespoke suiting client of ours has been reordering the same 100% cashmere flannel for five seasons. They pay a 10% deposit now because their reorder cycle is like clockwork. (Here I have to interject—that relationship did not happen overnight; we clawed our way to that trust level through dozens of spotless deliveries.)

But you must understand that even for the best partners, zero-deposit terms are practically non-existent in custom high-end textiles. Why? Because the factory’s balance sheet cannot carry the raw material liability entirely. Chinese manufacturing operates on thin margins and high volume. Our net profit on a meter of fabric might be 5% to 8%. Carrying 100% of the raw material cost for a 60-day production cycle destroys our working capital. My banking partners require a certain debt-to-equity ratio, and massive uncollateralized receivables from overseas buyers hurt that ratio. So when you negotiate, do not aim for "no deposit." Aim for "lower deposit plus faster final payment." You can offer to pay the balance not just before shipment, but within 5 days of the QC photo report being sent to you. That "early final payment" incentive is often more valuable to a factory than an extra 5% on the deposit, because it speeds up cash conversion.

What Are the Hidden Costs and Payment Gateways That Impact Your Final Invoice?

The price per meter on the proforma invoice is not the final cost of the fabric. That is a hard lesson that costs newcomers thousands of dollars. There are at least three hidden cost layers that you must account for before you make a bank transfer. The first is the international wire transfer fee. When you wire a 30% deposit from your US bank to our Chinese corporate account, intermediary banks take a bite—often $25 to $50 from your side, and another $15 to $25 from our receiving side. On a large invoice, this is negligible. On a small $2,000 deposit, it is a 2% hidden tax. The second is the foreign exchange conversion spread. Your bank does not convert USD to CNY at the Google exchange rate. They add a 2% to 4% margin above the interbank mid-rate. On a $50,000 order, that is a $1,000 to $2,000 invisible cost. I have seen small brands literally budget their fabric cost using Google’s exchange rate and then get surprised by a $1,500 shortfall.

The third and most insidious hidden cost is the "payment gateway intermediary" for alternative payment methods. Many Western buyers hate the rigidity of T/T (telegraphic transfer) wires and want to use PayPal, credit cards, or Alibaba Trade Assurance. I understand the desire for buyer protection. But these platforms charge the supplier a transaction fee. PayPal charges around 4.4% plus a fixed fee for international commercial transactions. Alibaba Trade Assurance charges a service fee of around 2% to 5% depending on the order volume and promotion. That fee is built into the price. If I quote you $10 per meter for a custom viscose georgette with T/T payment terms, and you demand PayPal, I will re-quote at $10.50 per meter to cover the fee. The buyer always pays the processing cost, either as a visible surcharge or an invisible price increase. I am brutally honest about this with clients. I ask them: "Do you want to pay the bank or pay the platform? Either way, the cost is yours."

How Do Bank Transfer Fees and Currency Exchange Spreads Inflate Your Fabric Cost?

The SWIFT international wire transfer network is a maze of intermediary correspondent banks. When you send a wire from your regional US bank, it goes through an intermediary bank like J.P. Morgan or Bank of America, then to a corresponding bank in China like Bank of China, and finally to our corporate account at a smaller commercial bank. Each intermediary takes a small "correspondent banking fee." Our payment instructions specifically say "Remitter to pay all charges," but many new buyers forget to check the box that says "OUR" under the field "Details of Charges." They select "BEN" (beneficiary pays) by mistake. That means all those $30 intermediary fees get deducted from the deposit that arrives in our account. If you owe us $5,000 as a 30% deposit and $4,920 arrives, our accountant will flag it, and the order does not start until the shortfall is settled. This is not pedantry; it is accounting integrity.

The currency risk is a separate beast. We quote in USD for most international clients because it is the lingua franca of global textile trade. But the factory economics operate in CNY. That means we have to estimate a forward exchange rate. If the USD strengthens against the CNY between the quote date and the payment date, we make a small forex gain. If the USD weakens, we lose margin. For large orders over $100,000, I sometimes lock in the exchange rate with a forward contract through our bank. But for smaller orders, we simply price in a 2% currency buffer into the quoted price. I tell my clients: if your order window is longer than 90 days, ask for an "exchange rate adjustment clause" in the contract. It protects both sides. If the USD moves more than 3% against the CNY, we split the difference. This prevents a scenario where a sudden currency swing makes the order unprofitable for the factory, which could lead to corner-cutting. Fair payment terms include forex realism.

Are Letter of Credit and Trade Assurance Worth the Extra Cost for High-End Custom Fabric?

A Letter of Credit is a 500-pound financial gorilla. It is a document issued by your bank guaranteeing payment to us once we present specific shipping documents. For a $200,000 order of custom cashmere coating, an L/C is standard and expected. It gives the buyer immense security—if we fail to ship on time or produce the correct documents, the bank does not release the funds. But for a $15,000 order of custom silk jacquard, an L/C is a nightmare of paperwork and bank charges. The issuing bank charges around 0.5% to 1% of the invoice value per month. If the L/C is open for three months, that is a 1.5% to 3% cost. Plus, there are discrepancy fees of $50 to $100 every time a document has a minor spelling error. I have seen shipments delayed by a week because the L/C said "Fumao Textiles" but the shipping document said "Shanghai Fumao Textiles International." That technical discrepancy gave the buyer’s bank the right to refuse payment. An L/C is security, but it is also a compliance weapon.

Alibaba Trade Assurance is a lighter, digital-first alternative. The buyer pays Alibaba, we ship the goods, and Alibaba releases funds to us after you confirm receipt. The protection is real—if the fabric is damaged or wildly off-spec, you can open a dispute and get a refund. The downside is the cost I mentioned earlier, plus the fact that the platform holds our cash for up to 30 days after you receive the goods. For a custom order where we have tied up our working capital in raw materials for 45 days, that additional 30-day hold is painful. I accept Trade Assurance for first-time small orders under $5,000 because it builds trust. For the fashion entrepreneur or startup who found me on Alibaba and wants to test the waters with a 200-meter custom organic cotton poplin, Trade Assurance is the right tool. But if you are placing a repeat order or a large custom development, I will gently steer you toward T/T with a milestone structure. The savings in platform fees alone can offset a portion of your shipping cost.

How Do You Protect Against Quality Dispute With Payment Leverage?

The most powerful quality control tool you possess is not a lab report or a third-party inspector. It is the final balance payment that is still in your bank account. That 70% or 50% you have not yet paid is the single greatest motivator for a factory to ensure every roll of custom fabric meets the specification you approved. I say this as a factory owner, and I want you to hear it: we want you to use that leverage. Not as a threat, but as a structured conflict resolution mechanism. A smart payment structure builds in a quality gate before the final transfer. At Shanghai Fumao, our standard procedure is to send you a detailed pre-shipment inspection report, including high-resolution photos of random roll openings, actual shade comparisons against your approved lab dip under a 6500K light box, and a summary of the AQL 2.5 inspection results. We send this package to you, and only after you acknowledge it in writing does our accountant issue the final invoice for payment. This protects you from "ship-and-hope" tactics.

But what happens if you discover a problem after receiving the report, or worse, after paying? I had a German sportswear client in 2022 who paid the 70% balance, and the shipment arrived. They found a subtle vertical stripe in a polyester pongee that was not visible in our inspection photos. This is where the post-payment relationship kicks in. They sent a field complaint with proof—a video of the fabric rolled out on their cutting table. Our QC team immediately pulled the retained sample from that dye lot and confirmed the defect was real. We offered a choice: a credit note against their next order for the faulty yardage, or a re-order at 50% discount to cover their cutting losses. They chose the credit note because they were already developing the next season. This resolution happened because our payment terms had established a baseline of mutual trust. We did not treat the final payment as "game over."

How Can a Retainage Clause in Payment Terms Save You From a Bad Batch?

A retainage clause—often called "retention money" in construction—is a provision where you hold back a small percentage of the total invoice, say 5% to 10%, until the goods arrive at your warehouse and you perform a final incoming inspection. This is common in large infrastructure contracts but surprisingly rare in textile sourcing. I am going to tell you why I actually recommend it for first-time custom orders over $30,000. That retained 5% sits in your account, earning you interest, and gives you absolute negotiating power if there is a latent defect that only reveals itself after shipment—like fabric shrinkage during your first pre-production wash, or color fastness failure on a specific trim. With a retainage clause, you say, "I am satisfied, the 5% is released after 14 days of receiving the goods and completing my internal QC." This gives you a 14-day safety window.

The factory’s perspective on retainage is mixed. We generally resist it because it extends our cash conversion cycle and creates accounting complexity. But if a client insists and the order value is substantial, I will agree with a clear, objective release trigger. The key is the release trigger must be binary and measurable, not subjective. You cannot say "I’ll release the 5% if I am happy." You must say ‘the 5% retainage will be released within 7 days unless a written defect notice with photographic evidence against the approved reference sample is provided.’ I drafted such a clause for a US luxury activewear client in 2024. They held back 5% on a $45,000 order of custom cupro jacquard. They found a minor shading issue on one roll out of 32. We negotiated a small deduction from the retainage—about $300—and released the remaining balance. The clause gave them the confidence to proceed without requiring an L/C for a complex custom order. It was a mature, professional compromise.

What Documentation Should You Demand Before Releasing Final Balance Payment?

You need a three-document minimum package before you hit send on that wire transfer. Document one is the signed and stamped pre-shipment inspection report from an independent third-party like SGS or ITS, or from Shanghai Fumao’s own CNAS lab if you trust the relationship. This report must detail the standard used (e.g., ANSI/ASQ Z1.4, Level II, AQL 2.5), the number of rolls inspected, the number of defects found per hundred units, and the overall pass/fail decision. Document two is the commercial invoice and packing list with exact roll numbers, weights, and yardage per roll that match the QC report. This prevents "QC inspected the good rolls, but shipped the bad ones." The roll numbers must cross-reference. Document three is what I call the "certified conformity pack": a set of physical lab test results for that specific finished lot, including shrinkage %, color fastness to rubbing (wet and dry), and tensile strength. These must be dated after the finishing date, proving they tested this actual batch, not a historical template.

I also advise buyers to ask for the "dye lot card." Every dyeing lot has a small retained swatch that the dyeing master keeps. Request a photo of your specific dye lot card held against the reference standard. If the final fabric looks different, that retained card is the forensic evidence. At Shanghai Fumao, we archive dye lot cards for 12 months by default. On one occasion, an Italian menswear brand disputed a midnight-blue wool blend color as being "too dark." We went back to the spectro reading of the dye lot card and the original approved lab dip. The dE (Delta E) value was 1.1—within the agreed tolerance of 1.5. The client was mixing the fabric with a lining that altered their visual perception. The dye lot card data resolved the dispute in five minutes without argument. Without that documentation, it would have been a "he-said, she-said" war ending in a chargeback.

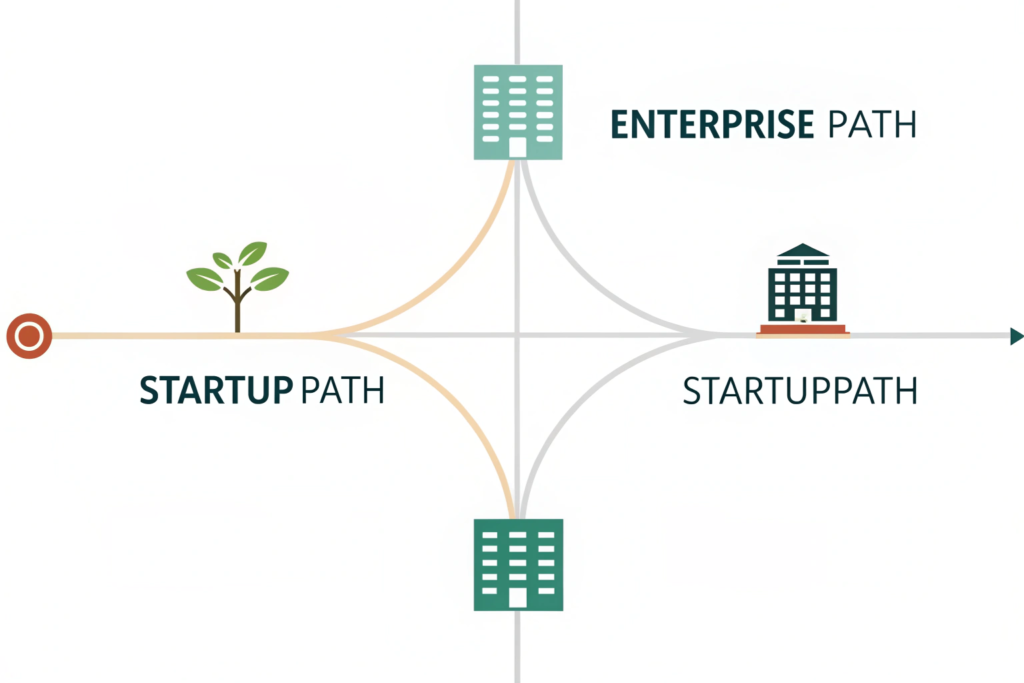

How Does Shanghai Fumao Structure Payment for Startups vs Enterprise Buyers?

A startup fashion brand with a $5,000 Kickstarter budget operates in a completely different financial solar system than a multinational retailer with a $500,000 seasonal restock. I cannot apply the same payment terms to both and expect either to succeed. The startup needs cash flow preservation and trust-building. The enterprise needs accounting convenience and bulk discounting. At Shanghai Fumao, we bifurcate our payment architecture to serve both ends of the spectrum without compromising our own financial safety. For startups and micro-brands doing first-stage custom development, I offer a lower deposit threshold combined with faster, smaller milestone payments. The goal is to make custom development accessible without exposing us to massive cancellation risk. For enterprise accounts with established trade history, we shift toward efficiency: cleaner invoice cycles, potential Net 30 terms for specific partners, and volume-based price adjustments that reflect the lower administrative overhead.

Let me give you the concrete structure. A startup asking for 300 meters of custom printed organic cotton for a capsule collection will likely see a 30% deposit to kick off the print strike-off process, a 20% payment upon strike-off approval and before bulk printing, and the 50% balance before shipment. The total order value might be $4,500. The three payments are small enough not to cripple their cash flow, but frequent enough to keep the project moving and the risk shared. An enterprise buyer ordering 15,000 meters of custom wool-poly suiting under a six-month contract will see a 30% deposit against the contract, then monthly running payments against actual shipments. This is called a "revolving credit" within the contract framework. They do not finance the entire contract upfront; they pay as we ship, based on the inspection approval for each release. This structure keeps the factory’s working capital cycling and aligns with the buyer’s budgetary cycles.

What Is the Minimum Order Quantity Threshold for Custom High-End Fabric at Fumao?

I have a philosophy I call "accessible custom." This means I work to lower the barrier for truly creative small brands to access high-end custom textile development. Our minimum order quantity for custom dyeing or printing on a woven base starts at around 300 meters per color. For complex jacquard development, where we must design and manufacture new dobby chains or jacquard cards, the minimum might be 500 meters due to the mechanical setup cost. But we do not enforce these minimums rigidly like a soulless bureaucracy. If you are a designer with a brilliant idea and you need only 150 meters of a specific custom linen-rayon blend, I will often accept the order if we can schedule it alongside a larger run of a similar base fabric. (I once squeezed a 120-meter custom order of silk noil for an artist into a dye lot overlap with a larger kimono fabric order—it worked because the dye bath was the same base color.)

The payment terms flex with the minimums. For sub-MOQ orders, the deposit percentage might be higher—closer to 50% or even 60%—because the unit cost of carrying that small-batch risk is disproportionately high. We also might charge a small "setup fee" of $200 to $500 for the lab dips if the order value is very low. I always explain this transparently. The setup fee is not profit; it covers the dyeing technician’s time and the chemicals used to formulate your unique shade. Once the bulk order proceeds, I usually deduct that setup fee from the final invoice. This way, the small brand pays only if they walk away after development. It incentivizes follow-through. I have seen too many artists request elaborate lab dip series with no intention of placing a bulk order. The small setup fee acts as a courtesy barrier to protect our sampling department’s resources.

Does Fumao Offer Net 30 or Open Account Terms for Established Wholesale Buyers?

I am going to be direct: open account terms, where we ship goods and wait 30 to 60 days for payment with no bank guarantee, are the platinum tier of textile trade relationships. They require a deep, multi-year history of flawless transactions, an audited financial statement from the buyer, and often a trade credit insurance policy that we purchase to cover the receivables. We do offer Net 30 terms to a very selective group of established enterprise buyers after a rigorous internal credit review. I typically require two years of clean trade history with Shanghai Fumao, with total order volume exceeding $300,000. One of our major European workwear brands operates on Net 30 after a 10% deposit against the seasonal contract. They provide us with a quarterly forecast, we reserve loom capacity, and we invoice them upon each partial shipment with a due date 30 days later. Their bank reference and Dun & Bradstreet report underwrote that decision.

For the vast majority of buyers, even fairly large ones placing $80,000 orders for the first time, Net 30 is not on the table immediately. But I do offer a bridge product: "Document against Payment" via the bank. This is a low-cost alternative to an L/C. We hand the original shipping documents—the bill of lading, which is the legal title to the goods—to our bank, who forwards them to your bank. Your bank releases the documents to you only after you pay. Until you pay, you cannot claim the container from the port. This gives you the assurance that the goods are real and shipped, and it gives us the assurance that we retain title until payment. The bank fees are modest—typically a flat document handling charge of $50 to $100. I recommend this option for mid-tier buyers who are outgrowing Trade Assurance but are not yet established enough for open account terms. It is a safe, traditional middle path.

Conclusion

Payment terms for custom high-end fabric are not just legal boilerplate; they are the circulatory system of your production partnership. They control the flow of cash from your bank account to the yarn supplier, the dye house, and the coating plant. The standard structure—a deposit to secure raw materials, with the balance tied to inspection milestones—protects both the buyer’s quality expectations and the factory’s survival. We walked through the hidden costs of wire transfers and platform fees, the power of retainage clauses and inspection documentation, and the very different approaches required for a small creative startup versus a seasoned enterprise buyer. The core insight is this: every payment term is a risk allocation tool. A high deposit allocates risk to the buyer. Open account terms allocate risk to the factory. The healthiest partnerships find the middle ground where risk is shared at each milestone, and the final balance is released only against objective lab data, not promises.

I built Shanghai Fumao’s payment architecture to be flexible but never naive. We want to fund your creative vision by buying the exact yarns you need and running the custom dyes you dreamed up, but we also must protect the 40 families whose livelihoods depend on our factory’s financial stability. That means being transparent about why deposits exist and honest about the fees we cannot absorb.

If you have a custom high-end fabric project in mind—something that requires a unique fiber blend, a proprietary color, or a technical performance finish—let us structure payment terms that make sense for your cash flow and our production reality. I am speaking from twenty years of making this work for brands of every size. Reach out to our Business Director, Elaine, at elaine@fumaoclothing.com. Tell her about your project, your timeline, and the payment structure you are hoping for. She will walk you through our standard terms and explore what flexibility we can offer based on your production volume and history. Let us build a financial architecture for your fabric that is as precise and durable as the textile itself.