Let me tell you the most dangerous lie in the textile industry. "Net 30."

Those two little words have bankrupted more promising fashion brands than any bad collection or missed trend. A brand places a $50,000 order for fabric. The supplier says "Payment terms are Net 30." The brand thinks "Great I have 30 days after I receive the fabric to pay." But that’s not how it works. Not even close.

Here’s the reality. The clock starts ticking when the fabric Leaves the Port in China . It spends 4 weeks on the water. It spends 1 week in customs. By the time the truck backs up to your warehouse door the invoice is already Overdue . The supplier is calling. The credit manager is threatening to hold your next order. You haven’t even cut the fabric yet and you’re already in Technical Default .

At Shanghai Fumao we’ve seen this movie play out a hundred times. We’ve also been on the other side of the table. We’ve had to extend credit to brands and we’ve had to chase payments. I understand the pressure from both ends.

The goal of this article is to change how you think about payment terms. They are not just an administrative detail. They are a Strategic Financial Tool . Negotiating the right terms can effectively Finance Your Inventory . Accepting the wrong terms can Strangle Your Cash Flow .

I’m going to give you the exact framework we use to structure fair sustainable payment agreements with our clients. This is how you keep your business solvent and your supplier relationship healthy.

What Is the Difference Between TT and LC Payment Methods

This is the first fork in the road for every fabric buyer. TT (Telegraphic Transfer) or LC (Letter of Credit) .

TT (Wire Transfer):

- What It Is: You send money directly from your bank account to the supplier’s bank account.

- Common Structure: 30% Deposit to start production. 70% Balance against Copy of Shipping Documents (Bill of Lading).

- Risk: High . You are paying the balance before you see the goods. If the supplier ships garbage you have very little recourse. You are relying entirely on Trust .

- Cost: Low. Bank fees are $25-$50 per transfer.

LC (Letter of Credit):

- What It Is: A Bank Guarantee . Your bank promises to pay the supplier’s bank only if the supplier presents Perfect Documents that meet the exact terms of the LC.

- Risk: Low . The bank acts as a Referee . If the documents are wrong (e.g., shipment date missed incorrect description) the bank Will Not Pay . The supplier is highly motivated to get it right.

- Cost: High. Bank fees can be 1-3% of the Invoice Value . It requires significant paperwork.

My Advice:

For orders under $20,000 TT is the industry standard. The bank fees for an LC eat up too much margin.

For orders over $50,000 or for a First Order with a new supplier an Irrevocable LC at Sight is worth the cost. It’s an insurance policy.

At Shanghai Fumao we accept both. We prefer TT for our long-term partners because it’s faster and cheaper for everyone. We encourage LC for new clients because it builds trust. We have nothing to hide so we welcome the scrutiny of the bank.

How Does a Deferred Payment LC Differ from a Sight LC

This is an advanced negotiation tactic for brands with Strong Banking Relationships .

Sight LC: The supplier gets paid Immediately when they present the correct documents to their bank. This is standard.

Deferred Payment LC (Usance LC): The supplier gets paid 30 60 or 90 Days AFTER they present the documents.

Why This Is Powerful:

You are effectively getting Interest-Free Financing from the supplier’s bank. The fabric arrives at your warehouse. You cut it sew it sell it and receive payment from your retail customers. Then you pay the bank.

This aligns your Cash Outflow with your Cash Inflow . It’s the holy grail of working capital management.

The Catch: The supplier must agree to wait for their money. Why would they do that? Only if they trust you implicitly or if you are a Major Account they cannot afford to lose. You can also offer to Split the Bank Interest Cost as a gesture of goodwill.

Why Are "Copy Docs" Payments Riskier Than They Seem

This is the trap I mentioned earlier. "70% Balance against Copy of Bill of Lading."

You receive an email with a scanned PDF of the Bill of Lading. It shows the container number and the sailing date. You wire $35,000.

Scenario A (Legitimate): The container arrives in 4 weeks. You pick it up. Everyone is happy.

Scenario B (Fraud): The Bill of Lading was Photoshopped . The container number is fake. The sailing date is fake. The supplier has your $35,000 and you have nothing. By the time you realize it the money is gone.

Scenario C (Dispute): The container arrives. You open it. The fabric is Wrong Color . But you already paid the 70% balance. You have lost all Leverage . The supplier has no financial incentive to fix the problem quickly. They will drag their feet on the credit note for months.

Mitigation Strategy: Always hold back 10-20% until After Delivery and Inspection . This is called "Retention Money." It keeps the supplier engaged in solving any post-delivery quality issues.

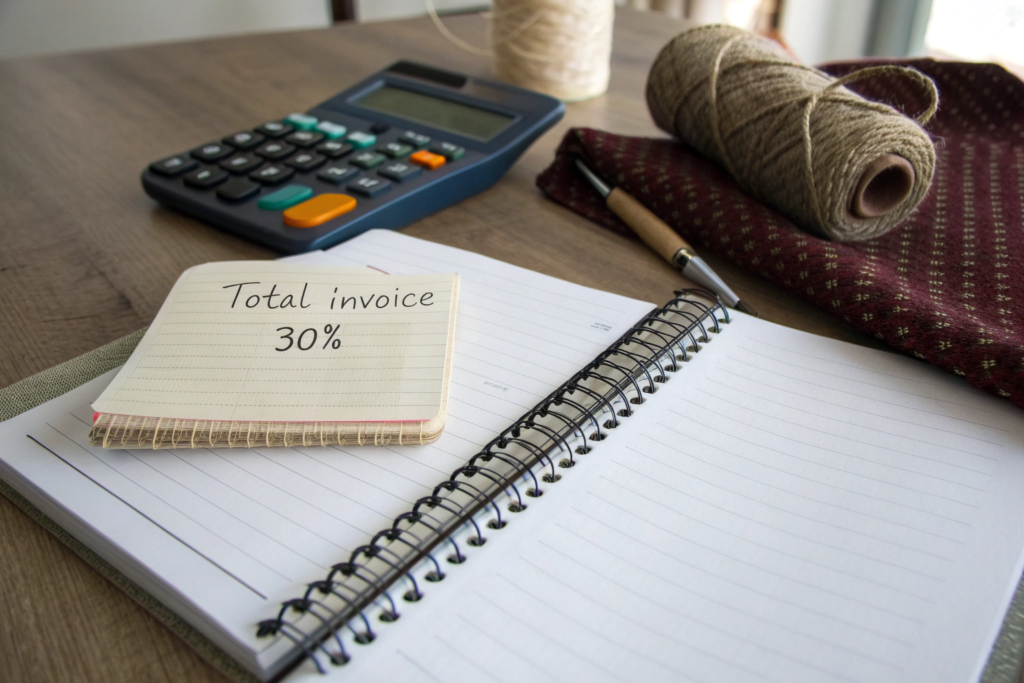

How to Negotiate a Deposit That Aligns with Raw Material Costs

The standard deposit is 30% . But where does that number come from? It’s not random. It’s roughly the Cost of Raw Materials .

When we receive a 30% deposit we use that money to buy Yarn . We don’t finance your yarn out of our own pocket. That’s the purpose of the deposit.

If you are ordering a Specialty Fabric that requires Expensive Imported Yarn (e.g., Cashmere Supima Cotton) the raw material cost might be 50-60% of the total cost. In this case a 30% deposit is Unfair to the Mill . We are financing your expensive yarn purchase.

How to Negotiate This:

Be transparent. Ask the supplier: "What is the actual cost of the raw yarn for this order?"

If the yarn is 50% of the cost offer to pay 50% Deposit . This shows you understand the business. It builds Massive Trust . In return for this higher deposit ask for:

- Faster Production Slot (You’ve covered their cash outlay they will prioritize you).

- Discounted Price (You’ve reduced their financial risk).

Conversely if you are ordering Stock Fabric that we already have on the shelf as greige goods the raw material cost is already sunk. The deposit is just to cover the Dyeing and Finishing cost (maybe 15-20% of total). In this case you can negotiate a Lower Deposit (e.g., 20% ) because the mill’s financial exposure is lower.

Why Is a Proforma Invoice Not a Legally Binding Contract

This is a crucial legal distinction that many small brands miss.

A Proforma Invoice (PI) is a Quotation . It’s a Preliminary Bill of Sale . It lists the goods the price and the terms. It is Not a Final Invoice .

It is Not Legally Enforceable in the same way a signed Sales Contract is.

If the price of yarn spikes by 20% between the PI and the Production Order the supplier can (and often does) come back and say "Sorry price increased."

Protect Yourself:

Ask the supplier to Stamp and Sign the Proforma Invoice and return it. In the email state clearly: "This stamped PI confirms the price and delivery date for PO #1234. Please confirm this price is firm for 30 days."

This creates a Paper Trail that is admissible in a dispute. It’s not a perfect contract but it’s better than a generic PDF.

How to Use Milestone Payments for Large Production Runs

For orders over $100,000 a simple 30/70 structure is too risky for both parties. You need Milestone Payments .

This breaks the order into Verifiable Stages . You pay as the work is completed. This reduces the buyer’s risk of total loss and provides the supplier with Working Capital throughout the process.

Example Milestone Schedule for a 10,000-Yard Woven Order:

| Milestone | Deliverable | Payment | Cumulative Paid |

|---|---|---|---|

| 1. Yarn Purchase | Copy of Yarn Invoice | 20% | 20% |

| 2. Weaving Complete | Photo of Greige Rolls | 30% | 50% |

| 3. Dyeing Complete | Lab Dip Approval | 30% | 80% |

| 4. Shipment Ready | Final Inspection Report | 15% | 95% |

| 5. Delivery | POD Signed | 5% | 100% |

This structure aligns everyone’s interests. The supplier gets cash flow to pay for yarn and labor. You get Proof of Progress before you release more funds.

How to Structure Letters of Credit to Avoid Discrepancies

An LC is a powerful tool but it is a Blunt Instrument . It operates on the principle of Strict Compliance . If the documents presented by the supplier do not Exactly Match the terms of the LC the bank Will Reject them.

This is called a Discrepancy . Each discrepancy costs $75 – $150 in bank fees. And it delays the shipment.

The Most Common Discrepancies (And How to Avoid Them):

-

Description of Goods: The LC says "100% Cotton Twill Fabric." The invoice says "Cotton Twill Fabric." Discrepancy. The word "100%" is missing. Fix: Copy and paste the exact description from the LC into every document.

-

Spelling Errors: The LC says "Shanghai Fumao Textile." The Bill of Lading says "Shanghai Fumao Textiles." Discrepancy. Fix: Proofread like a hawk.

-

Late Shipment: The LC says "Latest Shipment Date: 2026-05-30." The Bill of Lading shows an On-Board Date of 2026-05-31. Discrepancy. The bank will Not Pay unless the LC is amended. Fix: Build a 5-Day Buffer into the LC expiry date.

-

Inconsistent Weights: The Packing List shows Net Weight 500kg . The Bill of Lading shows Gross Weight 550kg (includes pallet). The LC asks for Net Weight . Discrepancy. Fix: Ensure all weight declarations match the exact term specified in the LC.

At Shanghai Fumao we have a dedicated documentation specialist who checks every LC document against the original LC text before it goes to the bank. This one person saves our clients thousands of dollars a year in discrepancy fees.

What Is a "Soft Clause" and Why Should Buyers Avoid Them

A Soft Clause is a sneaky condition inserted into an LC that makes payment Contingent on the Buyer’s Approval .

Example of a Soft Clause:

"Payment requires presentation of an Inspection Certificate signed by the Buyer’s Representative."

The Danger: The buyer can simply Refuse to Sign the inspection certificate. The supplier cannot get paid. This is Bad Faith . If you use this clause to strong-arm a supplier you will destroy the relationship and they will never work with you again.

Legitimate Alternative: Use Third-Party Inspection (SGS Intertek). The LC requires a certificate from the Independent Lab . This protects the buyer from bad quality but it’s Objective . The supplier knows they can meet the standard.

How to Amend an LC Without Delaying the Shipment

You realize the LC has a typo in the port of discharge. The fabric is ready to ship. Do not ship against a faulty LC.

Contact your bank immediately and request an LC Amendment . The bank will send a SWIFT Message to the supplier’s bank. This takes 2-3 Business Days .

Critical Tip: Instruct the supplier "Do Not Ship Until Amendment Received." If they ship before the amendment is received and the documents are presented with the discrepancy they will be rejected. The cargo will arrive at the port with No Documents . This is a logistical nightmare.

What Are Fair Penalties for Late Delivery in Fabric Contracts

Delays happen. But there must be Consequences or there is no incentive to perform.

The industry standard for a fair late delivery penalty is Liquidated Damages .

The Clause:

"In the event of a delay exceeding 14 days from the agreed shipment date the Buyer is entitled to a discount of 0.5% of the invoice value per week of delay up to a maximum of 5% of the total invoice value ."

Why This Works:

- It’s Not Punitive. 0.5% per week is not enough to bankrupt the supplier. It’s a Nudge .

- It’s Capped. The maximum 5% protects the supplier from catastrophic liability.

- It Compensates the Buyer. You likely had to offer a discount to your own retail customers to keep them happy. This clause covers that cost.

What to Avoid: "Time is of the Essence." This legal phrase allows you to Cancel the Order Entirely and sue for damages. It’s a Nuclear Option . If you use this clause a supplier will either refuse the order or build a massive risk premium into the price. It’s not worth it unless you are dealing with a Wedding Dress or a Movie Premiere .

How to Draft a Force Majeure Clause That Is Actually Fair

COVID taught us that Force Majeure (Act of God) matters.

A supplier’s standard Force Majeure clause will be Very Broad . "Supplier is not liable for delays caused by… government action pandemic raw material shortage…"

This is a Get Out of Jail Free Card .

Negotiate a Fairer Version:

"Supplier shall notify Buyer of a Force Majeure event within 48 Hours . If the delay exceeds 30 Days Buyer has the right to Cancel the Unshipped Balance without penalty."

This prevents the supplier from holding your order hostage indefinitely. It allows you to source alternative fabric if the delay is extreme.

Why Is a Discount Better Than a Credit Note for Cash Flow

If there is a minor quality issue (e.g., 5% of rolls have a slight shade variation) the supplier will offer a Credit Note against your Next Order .

Refuse This. Politely but firmly.

Ask for a Discount on the Current Invoice .

The Math:

Credit Note: You have to spend Another $10,000 to save $500. That’s Negative Cash Flow .

Discount: You pay $500 Less right now. That’s Positive Cash Flow .

Always take the Cash Discount . If the supplier refuses offer to split the difference: "Okay I’ll take 50% as a discount now and 50% as a credit note." This shows you are willing to compromise.

Conclusion

Negotiating payment terms is one of the most impactful yet overlooked skills in fabric sourcing. The terms you agree upon dictate your working capital your risk exposure and the fundamental dynamics of your supplier relationship. By understanding the mechanics of TTs and LCs by aligning deposits with material costs and by structuring fair penalty clauses you can protect your cash flow while still being a valued partner to your mill.

The goal is not to squeeze every last concession out of your supplier. The goal is to create a Sustainable Financial Framework that allows both businesses to thrive. A supplier who is paid fairly and on time will prioritize your orders and advocate for your brand.

At Shanghai Fumao we believe in transparent and fair financial dealings. We work with our clients to find payment structures that support their growth cycles. We are not a bank but we understand that our success is tied to your financial health.

If you are planning a production run and want to discuss payment options that align with your business model please reach out to our Business Director Elaine. She can explain our standard terms and explore alternative structures for larger strategic partnerships.

Contact Elaine at: elaine@fumaoclothing.com