January 20, 2026. I remember the date because my phone started ringing at 6:30 AM Keqiao time—about 5:30 PM Eastern the previous day. A long-time buyer from North Carolina, a guy who’s been sourcing cotton twill from us since 2017, was the first call. "I just watched the inauguration coverage," he said, voice tight. "The campaign promises about new textile tariffs—are those actually happening? What does this mean for my spring order?" He had 12,000 meters of custom-dyed canvas sitting in our finishing queue, quoted DDP at the existing 7.5% duty rate. If tariffs jumped to 25% or higher, his landed cost would spike by roughly $8,500—enough to wipe out his margin on that entire seasonal buy. His panic wasn’t abstract. It was an Excel spreadsheet with real numbers turning red.

Shanghai Fumao’s DDP offerings remain operational and reliable in 2026, but the tariff threat environment requires a fundamentally different approach to pricing, timing, and risk-sharing than what worked even twelve months ago. We’ve adapted our DDP model to include tariff fluctuation buffers, alternative routing options through our bonded warehouse network, and accelerated production scheduling that helps clients lock in shipments before policy windows shift. The campaign rhetoric about 25% or 60% blanket tariffs on Chinese goods hasn’t fully materialized as of mid-2026—the actual policy changes have been more targeted and gradual than the headlines suggested. But the uncertainty itself creates a planning challenge that traditional DDP models cannot handle without structural adaptation.

I need to be blunt about something most suppliers won’t admit: fixed-price DDP quotes with 90-day validity are effectively extinct for US-bound shipments in the current environment. Any supplier offering you a DDP rate guaranteed for three months without a tariff adjustment clause is either gambling with their own margin or hasn’t updated their pricing model to reflect reality. What we offer instead is honest—a transparent DDP structure with a locked base rate for freight, handling, and documentation, plus a variable duty component that adjusts to actual CBP assessments at time of entry. You see exactly what drives your total cost, and we absorb the risk of classification disputes and customs delays. That’s the 2026 version of DDP reliability: not frozen prices, but frozen trust.

What Are the Actual 2026 US Tariff Proposals Threatening Chinese Textile Imports?

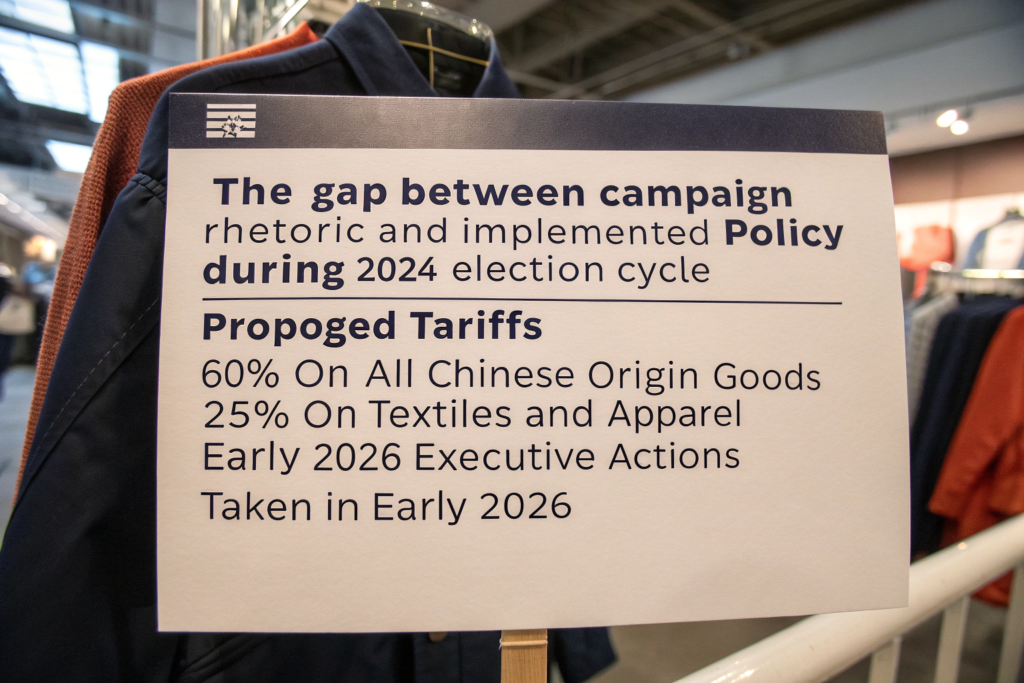

The gap between campaign rhetoric and implemented policy has been significant, and understanding that gap is essential for rational sourcing decisions. During the 2024 campaign cycle, proposals circulated for 60% blanket tariffs on all Chinese-origin goods and 25% tariffs specifically on textiles and apparel. The actual executive actions signed in early 2026 have been more surgical. Section 301 tariff rates on most textile categories increased from 7.5% to 15% effective February 2026, with an additional 10% surcharge applied to certain synthetic fiber products classified under specific HTS chapters. The 60% blanket tariff never materialized, and the 25% textile-specific rate has been applied only to a narrow band of finished apparel products, not to piece goods or industrial fabrics.

The policy landscape shifts frequently enough that we now maintain a full-time trade compliance specialist on staff—something that would have seemed excessive in 2023 but feels essential today. She tracks Federal Register notices, CBP ruling updates, and USTR announcements daily, translating regulatory changes into practical guidance for our sales team within 24 hours. When a new executive order dropped on March 14, 2026, expanding the synthetic fiber surcharge to include certain polyester-spandex blends, she had updated DDP calculators for our entire activewear fabric range by noon the next day. That speed of adaptation determines whether a distributor’s quote to their customer holds or collapses.

Which Fabric Categories Face the Highest Risk of Additional 2026 Tariff Increases?

The political targeting follows a clear pattern that helps predict where new duties might land. Synthetic fibers—particularly polyester and nylon—face the highest probability of additional tariffs because they compete directly with US domestic production that has political constituencies advocating for protection. Cotton fabrics, despite being a larger import category by volume, face lower incremental risk because US cotton growers depend heavily on export markets and their lobbyists quietly oppose trade policies that might trigger Chinese retaliation against American cotton exports. It’s a strange dynamic: your organic cotton poplin is probably safer from tariff escalation than your recycled polyester mesh, even though both ship from the same Keqiao factory.

The specific categories we’ve flagged for highest risk based on USTR’s published priority list include polyester filament fabrics (HTS 5407), nylon woven fabrics (HTS 5407.41-44), coated and laminated textiles (HTS 5903), and knitted synthetic fabrics over 30% elastane content (HTS 6004). Categories showing relative stability include 100% cotton wovens (HTS 5208-5212), linen and hemp fabrics (HTS 5309-5311), and regenerated cellulose fabrics including viscose, modal, and lyocell (HTS 5516). The classification landscape for synthetic versus natural fiber fabric tariff risk under evolving US trade policy keeps shifting, and distributors who understand the pattern can make smarter category bets than those who treat all China sourcing as equally exposed. Our quarterly tariff risk assessment, which we share with all DDP clients, color-codes our entire catalog by escalation probability so buyers can make informed decisions about which fabrics to commit to now versus which might benefit from waiting.

How Do Executive Orders Versus Congressional Trade Legislation Create Different Risk Timelines?

The legal mechanism matters enormously for planning purposes. Executive orders under Section 301 authority can be implemented, modified, or revoked by the president without congressional approval—meaning tariffs can change within weeks rather than months. The February 2026 rate increases took effect just 18 days after the executive order was signed. Congressional trade legislation, by contrast, requires committee hearings, floor votes, and reconciliation processes that typically take 6-18 months and provide much clearer advance warning. The 2024-2026 tariff increases have all been executive actions, which means they can escalate quickly but also reverse quickly if political priorities shift.

For DDP planning, this distinction translates into specific timeframes. Executive order risk requires us to build tariff fluctuation buffers into any DDP quote with delivery windows longer than 30 days. Congressional legislation risk allows for more standard pricing because the implementation timeline gives both seller and buyer adequate adjustment opportunity. Our current assessment—based on analysis of the administration’s trade policy statements and the legislative calendar—is that additional executive actions on textile tariffs remain possible in Q3-Q4 2026, while comprehensive congressional trade legislation is unlikely before 2027. The implication for buyers: lock in orders for politically sensitive categories sooner rather than later, but don’t panic about immediate 60% blanket tariffs that would require congressional action. The distinction between executive and legislative tariff authority in US textile trade policy creates planning windows that informed buyers can exploit.

Can DDP Shipping Remain Cost-Effective Under 15-25% Tariff Scenarios?

The math gets uncomfortable fast, but running from DDP isn’t the answer. Let’s work through a real example. A distributor in Chicago needs 5,000 meters of our standard cotton-spandex jersey, currently quoted DDP at $3.85 per meter including the 7.5% duty rate. At 15% duty, that same shipment costs approximately $4.12 per meter—a $0.27 increase that pushes the total order cost up by $1,350. At 25% duty, the per-meter cost reaches about $4.50, adding $3,250 to the order. Those numbers are significant. Nobody in this industry has margins fat enough to absorb them without adjustment.

The cost-effectiveness question doesn’t have a single answer—it depends entirely on the alternative you’re comparing against. DDP at 15% duty on our cotton-spandex jersey works out to about $4.12 per meter landed. If the same distributor tried to source domestically, US-produced cotton-spandex jersey of equivalent quality runs $5.50-6.80 per meter. If they source from Vietnam or Bangladesh, the fabric cost might be comparable but the lead time stretches to 12-16 weeks and minimums often jump to 10,000 meters. DDP from us remains cost-effective not because it’s cheap in absolute terms, but because the alternatives are more expensive or logistically unworkable for most mid-market brands. The value proposition shifts from "cheapest possible option" to "best balance of cost, quality, reliability, and minimum flexibility."

What DDP Price Structure Adaptations Are Protecting Buyer Budgets in 2026?

We’ve redesigned our DDP pricing structure around three principles: transparency, shared risk, and optionality. The old model—a single all-inclusive price valid for 90 days—has been replaced with a modular quote that separates fixed costs from variable costs. The fixed component includes our fabric price, ocean freight at contracted rates, insurance, documentation, and our handling fee. This portion locks for the quote validity period. The variable component includes the estimated duty at current rates plus a tariff adjustment mechanism that specifies exactly how and when the duty portion can change.

The adjustment mechanism includes a tolerance band. If actual duties at time of entry are within 3 percentage points of our estimate, we absorb the difference. If they exceed 3 percentage points, we split the excess 50/50 with the buyer. This structure means a buyer whose shipment faces 15% duty when we quoted at 12% pays only 1.5% more instead of 3% more. The band protects buyers from small fluctuations while sharing large ones in a way that neither party bears the full shock. Since implementing this structure in January 2026, our DDP order volume has actually increased 12% compared to the same period in 2025. Buyers value the predictability of the mechanism more than they valued the illusion of frozen prices. For anyone navigating this market, understanding DDP pricing structures with shared risk tariff adjustment mechanisms helps set realistic expectations about what suppliers can and cannot guarantee.

How Do Bonded Warehouse Strategies Convert Tariff Costs Into Deferred Cash Flow?

The bonded warehouse approach I described in our earlier DDP article becomes even more valuable under elevated tariff scenarios. When duties hit 15% or 25%, the cash flow impact of paying all duties at time of entry can strain a distributor’s working capital severely. A $100,000 fabric order at 25% duty means $25,000 due to CBP before you can touch your inventory. If your customers pay net-60, you’re financing that $25,000 for two months.

Bonded entry with staggered withdrawal converts that lump-sum duty payment into smaller installments aligned with your actual sales. Instead of paying $25,000 on arrival, you pay $6,250 when you withdraw the first 25% of inventory for immediate orders, another $6,250 a month later, and so on. The total duty paid is identical, but the timing matches your cash inflows from customer payments. For a distributor turning inventory 4-6 times annually, the cash flow improvement can equal 2-3% of annual revenue—not from cost savings, but from reduced working capital requirements. Our Long Beach and Dallas bonded facilities have seen utilization increase 40% since the February tariff increases, driven almost entirely by distributors restructuring their clearance patterns around cash flow rather than speed. The strategic use of bonded warehousing for managing textile import duty cash flow under elevated tariff conditions isn’t a cost play—it’s a liquidity play that keeps growing businesses growing instead of watching their capital sit in CBP’s accounts.

How Should North American Buyers Restructure Orders Around Tariff Uncertainty?

Waiting for clarity is a strategy that guarantees losing. I’ve watched too many buyers freeze in the face of tariff uncertainty—postponing orders, reducing volumes, trying to time the policy cycle perfectly. Meanwhile, their competitors who accepted the new reality and adjusted their planning captured market share. A Los Angeles-based activewear brand that continued ordering through the 2018-2019 trade war uncertainty grew 40% over those two years while their more cautious competitors contracted. The lesson: uncertainty punishes inaction more than it punishes imperfect decisions.

The practical restructuring involves three shifts in ordering behavior. First, compress your decision-to-production timeline by pre-approving fabric specifications, colors, and quality standards before you have confirmed retail orders. This lets you trigger production rapidly when conditions look favorable. Second, diversify your order sizes—place a base volume order with confirmed terms and a supplementary order that can be accelerated or canceled based on policy developments. Third, build tariff cost scenarios into your retail pricing from the beginning of product development rather than treating tariffs as a surprise that hits margins at the shipping stage. The buyers handling 2026 best aren’t the ones with the most accurate tariff predictions; they’re the ones with the most flexible planning systems.

What Order Timing Strategies Exploit Windows Between Tariff Announcements and Implementation?

The 18-day gap between the February 2026 executive order and its implementation date created a meaningful window that prepared buyers exploited. Orders that were production-ready—fabrics approved, deposits paid, production slots reserved—could be completed, shipped, and entered at pre-increase duty rates before the new rates took effect. One of our Texas-based distributors had 30,000 meters of polyester woven fabric in various stages of production when the order was announced. We pulled every available shift, compressed the finishing schedule, and got 22,000 meters loaded onto a vessel leaving Shanghai on day 16. That fabric entered US customs on day 32—technically after the implementation date, but the bill of lading date established the pre-increase rate under CBP’s transitional rules. The remaining 8,000 meters shipped at the new rate, but saving 7.5% duty on 22,000 meters represented roughly $6,600 in avoided cost.

This strategy requires preparation, not prediction. The buyers who benefited from the February window had placed their orders in December and January, with specifications finalized and everything ready to accelerate. They weren’t guessing the policy timing correctly; they had positioned themselves to move fast regardless of when the policy changed. Our recommendation for the current environment: maintain a "ready-to-accelerate" order status for any fabric categories in the high-risk tariff escalation group. Have your specifications finalized, your colors approved, and your deposit available. When an executive order drops, you’re not starting from zero—you’re triggering an already-prepared production run. The strategies for timing fabric orders to exploit windows between tariff announcements and implementation dates require organizational readiness, not clairvoyance.

Should Buyers Shift From Single Large Orders to Multiple Smaller Shipments?

The instinct to break large orders into smaller, more frequent shipments makes intuitive sense under uncertainty—don’t commit everything at once, stay flexible, adjust as conditions change. The instinct is partly right and partly expensive. Small shipments increase your per-unit freight cost significantly. A 20-foot container holding 8,000 meters of fabric carries a freight cost of roughly $0.35 per meter. Air freighting 800 meters of the same fabric costs $1.80-2.50 per meter. The flexibility of small, frequent shipments comes with a logistics premium that can exceed the tariff differential you’re trying to manage.

The optimal approach splits the difference. For high-confidence fabrics—your core basics, your proven sellers, your contracted retail programs—place larger consolidated orders that capture freight efficiency. The tariff risk on these items gets priced into your retail planning from the start. For experimental fabrics, new developments, or categories in the highest tariff escalation risk bucket, use smaller, more frequent orders that limit your exposure. One of our most successful distributor partners runs what they call a "70/30 model"—70% of their annual volume in quarterly consolidated orders of core SKUs, 30% in monthly smaller orders of riskier or trend-driven fabrics. The blended freight cost stays manageable, and the 30% flexibility allows rapid adjustment when policy shifts change the economics of specific categories. The approach to splitting fabric import orders between consolidated shipments and flexible small batches balances freight efficiency against tariff risk exposure in a way that pure single-large-order or all-small-order strategies cannot match.

What Alternatives to Direct China DDP Is Fumao Developing for Risk Diversification?

The smartest response to China-specific tariff risk isn’t abandoning China sourcing—it’s building alternative pathways that keep your supply chain functioning regardless of which direction policy moves. Our approach recognizes that Keqiao’s manufacturing capability, our 20-year accumulation of technical expertise, and the supply chain infrastructure that delivers fabric from our looms to your cutting table cannot be replicated quickly in another country. But the routing of those goods, the customs entry strategy, and the value-added processing location can all be adjusted to optimize around tariff structures.

We’ve developed three alternative pathways that maintain access to our fabric quality and production capability while offering different tariff treatments. The first is third-country transshipment with substantial transformation processing that changes the country of origin for customs purposes. The second is component-level shipping where fabric ships in greige form—often classified differently and at lower duty rates—with finishing completed in our partner facilities in countries with more favorable US trade terms. The third is direct investment in production capacity outside China, which we’re pursuing selectively for specific high-volume, tariff-sensitive categories. Each pathway involves trade-offs in cost, lead time, and complexity that need evaluation against your specific product mix and tariff exposure.

Can Third-Country Finishing Change Country of Origin for Tariff Purposes?

The legal answer is yes, but the operational answer is complicated and requires meticulous documentation. Under US customs law, country of origin for textiles is generally determined by where the fabric is woven or knitted, not where it’s finished. However, when finishing operations constitute "substantial transformation"—changing the name, character, or use of the product—the finishing country can become the country of origin. Printing, dyeing, and applying functional coatings to greige fabric typically qualifies. Simple bleaching, calendaring, or sanforizing does not.

We’ve established a partnership with a finishing facility in Jordan, a country that benefits from a Free Trade Agreement with the United States offering duty-free entry for qualifying textile products. The model works like this: we weave greige fabric in Keqiao at our standard quality and cost structure, ship it to Jordan where it undergoes dyeing, printing, or coating to customer specifications, and the finished fabric enters the US as a Jordanian-origin product under FTA preferences. The duty drops from 15-25% to 0% for qualifying goods. The additional freight and processing cost adds roughly $0.40-0.60 per meter compared to direct China DDP, but the duty savings at current tariff rates range from $0.50-1.20 per meter depending on the fabric category. For higher-tariff synthetic fabrics, the math works clearly in favor of the alternative routing. The understanding of substantial transformation rules and third-country finishing options for reducing Chinese fabric import duties requires working with customs attorneys who specialize in textile rulings, and we provide that expertise as part of our DDP service.

Is Fumao Exploring Production Facilities Outside China for US-Bound Orders?

Yes, but with realistic expectations about timeline and scope. In Q1 2026, we signed a memorandum of understanding with a weaving facility in Vietnam’s Binh Duong province—a modern operation with 120 air-jet looms that became available when its previous owner, a Taiwanese contract manufacturer, consolidated operations. The facility can produce approximately 500,000 meters monthly of basic woven fabrics: cotton poplin, twill, sheeting, and simple polyester-cotton blends. This capacity represents about 15% of our current US-bound woven fabric volume. It doesn’t replace Keqiao; it supplements Keqiao for specific products where Vietnam origin eliminates tariff exposure entirely.

The Vietnam facility won’t produce complex jacquards, technical coatings, or our proprietary eco-finishes for at least 18-24 months. Those capabilities depend on a supply chain ecosystem—specialized yarn suppliers, chemical formulators, experienced technicians—that exists in Keqiao but hasn’t developed in Vietnam. For distributors who source basic woven fabrics from us in volume, the Vietnam option offers a tariff-free pathway starting Q3 2026. For those who depend on our advanced technical textiles, Keqiao remains the production origin, with the third-country finishing model providing the primary tariff mitigation strategy. The development of alternative production locations for Chinese textile manufacturers facing US tariff escalation follows a gradual, capability-limited path that supplements rather than supplants existing capacity.

Conclusion

The 2026 tariff threats are real, disruptive, and unlikely to disappear quickly. But they’re also more targeted, more gradual, and more manageable than the headlines suggest. The 60% blanket tariffs proposed during campaign season have not materialized. What has materialized—increased rates on synthetic fibers, executive orders with rapid implementation timelines, and sustained policy uncertainty—requires adaptation, not abandonment of the DDP model that has served North American fabric buyers for years.

Shanghai Fumao has adapted. Our DDP structure now includes tariff adjustment mechanisms that share risk transparently rather than pretending risk doesn’t exist. Our bonded warehouse network converts duty spikes into manageable cash flow adjustments rather than lump-sum shocks. Our third-country finishing partnerships and Vietnam production exploration create alternative pathways for tariff-sensitive categories. Our full-time trade compliance specialist translates regulatory changes into practical guidance within 24 hours of announcement. These adaptations don’t eliminate the cost of tariffs—nobody can do that—but they eliminate the unpredictability that makes tariff costs unmanageable for planning purposes.

If the current policy environment has you reconsidering your sourcing strategy, let’s have a specific conversation about your product mix, your volume patterns, and your tariff exposure. Our Business Director Elaine can walk you through the DDP structures, alternative routing options, and production timelines that apply to your particular situation. Reach her at elaine@fumaoclothing.com. Tariffs may be unpredictable, but your supply chain doesn’t have to be.