Let's kill the fantasy right now. You cannot "avoid" US tariffs on Chinese fabric imports in 2026 the way you avoid a pothole on the road. The tariffs—specifically the Section 301 additional duties on a wide range of textiles from China—are the law. Attempting to evade them by misclassifying goods, undervaluing shipments, transshipping through a third country, or simply hoping your container isn't inspected is not a strategy; it's a felony. US Customs and Border Protection (CBP) has dramatically increased its enforcement capacity, its data analytics, and its coordination with foreign customs agencies. They are catching evaders, and the penalties include seizure of the goods, fines up to the domestic value of the merchandise, and a permanent red flag on your importer record that will haunt every future shipment. The pain of getting caught is not a financial risk you manage; it's a business-ending event.

But—and this is the most important "but" in this entire article—you can legally and significantly minimize your tariff burden. There is a profound difference between illegal evasion and strategic, legal minimization. At Shanghai Fumao, we help our US clients reduce their effective tariff rate by 50%, 70%, or even 100% on specific products, using tools that are built into the trade system: correct tariff classification, raw material origin analysis, First Sale for Export valuation, and legitimate trade preference programs. These are not loopholes. They are codified in the Harmonized Tariff Schedule and CBP regulations. They require rigorous documentation, supply chain transparency, and a willingness to do the paperwork that less sophisticated suppliers avoid.

I'm going to walk you through the exact, legal tariff minimization strategies that our most successful US importers use in 2026. I'll show you how the HTS code is a decision, not a given, and how getting it right can save you 10-15% on the spot. I'll explain how the origin of the flax fiber in your cotton-linen blend can be the key to unlocking a zero-duty rate. And I'll detail the documentation you must have—not should have, must have—to survive a CBP audit and prove that your low tariff rate is legitimate. This is not about hiding from the tariff. It's about mastering the system.

How Does HTS Classification Legally Reduce Fabric Tariffs?

The single most powerful tariff minimization tool available to every fabric importer is also the most misunderstood: the HTS code. The Harmonized Tariff Schedule of the United States is not a simple list where "cotton fabric" equals one code and one duty rate. It's a hierarchical, legal text where the exact fiber composition, the weave structure, the weight, the width, and even the intended end-use can shift a product from a high-duty classification to a low-duty one. Misclassification is a risk. Correct, optimal classification within the legal framework is a skill.

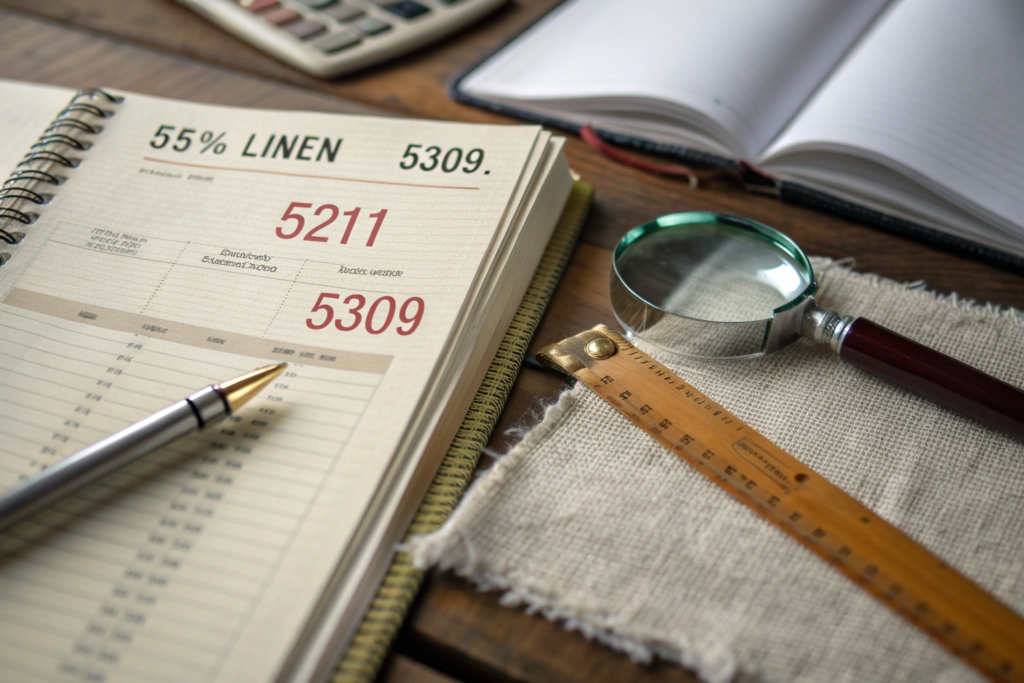

Let me give you a concrete, real-world example from our product line. Our SL-550 fabric is a 55% European flax linen, 45% BCI cotton blend, woven into a plain weave, at 180 GSM. The correct HTS classification for this fabric is 5309.19.9000, which covers woven fabrics of flax containing 85% or less by weight of flax, unbleached or bleached, other. The general rate of duty for this code is 2.9% ad valorem. Now, if a buyer or a customs broker misclassifies this exact same fabric under a cotton-based heading—say, 5211.19.0020, for woven fabrics of cotton containing less than 85% cotton, mixed mainly with man-made fibers—they would face a duty rate of 7.4% ad valorem, plus potentially a different Section 301 tariff treatment. The fabric hasn't changed. The fibers haven't changed. But a 4.5% duty difference has been created by classification error.

The correct classification of a cotton-linen blend depends on the legal principle of "predominance by weight." If the fabric is 55% flax and 45% cotton, flax predominates, and the fabric is classified under the flax heading (Chapter 53). If the fabric were 55% cotton and 45% flax, cotton would predominate, and it would be classified under the cotton heading (Chapter 52). This is not a matter of opinion; it's a legally defined rule in the General Rules of Interpretation (GRI) of the HTS.

The strategic opportunity lies in the fiber blend design itself. When we develop a custom cotton-linen blend with a client, the choice between a 55/45 ratio and a 45/55 ratio is not just aesthetic or functional. It's a tariff decision. By designing the blend to be flax-predominant, you shift into a different HTS chapter with a different—often lower—base duty rate. This is legal tariff engineering, and it's something we discuss openly with clients during the development phase. A New York-based converter who buys our SL-550 by the container-load was initially classifying his linen-cotton imports under a cotton heading out of habit. His customs broker suggested the switch to the flax heading, backed by our mill certification proving the 55% flax content. The reclassification saved him an estimated $18,000 in duties in the first year alone. No laws were broken. No forms were hidden. The correct classification was simply applied. For a deeper understanding, reading the official US Harmonized Tariff Schedule for Chapters 52 (Cotton) and 53 (Flax), including the Section Notes that define the scope of each heading and the legal rules for classifying mixed-fiber fabrics is the essential primary source, and consulting CBP's Informed Compliance Publications on textile classification, which provide detailed guidance on how to correctly classify woven fabrics based on fiber composition and construction is a professional necessity for anyone serious about tariff optimization.

What Is the "First Sale" Rule and Can It Apply to Fabric?

The "First Sale for Export" rule is a legitimate, CBP-recognized valuation method that can reduce the customs value of imported goods—and therefore the duties paid—by basing the transaction value on an earlier sale in the supply chain, rather than the final sale to the US importer. It's complex, it's not always applicable, and it requires meticulous documentation, but when it works, the duty savings can be substantial.

Here's how it applies in a textile context. In a typical fabric supply chain, there are multiple transactions. A trading company buys fabric from a mill. The mill sells to the trading company at one price (the "first sale" price). The trading company then sells to the US importer at a higher price (the final sale price). Under standard valuation, the customs value is the price paid by the US importer to the trading company—the final sale price. Duties are calculated on this higher amount.

Under First Sale valuation, if specific conditions are met, the customs value can be based on the price paid by the trading company to the mill—the "first sale" price—which is lower. The duties are then calculated on this lower amount. The conditions are that the first sale must be a bona fide, arm's-length transaction, the goods must be clearly destined for export to the US at the time of the first sale, and the importer must be able to provide CBP with complete documentation of both transactions, including the factory's invoice to the trading company.

For a US importer buying directly from a manufacturer like Shanghai Fumao, where there is no intermediary trading company, First Sale is generally not applicable. The importer is buying directly from the mill; there is no "earlier" sale. However, if you are buying from a Chinese trading company, or if you are a large brand sourcing through a buying office, First Sale could be a viable duty reduction strategy. You are effectively stripping out the middleman's markup from the customs valuation.

A large US apparel brand that sources fabric through a Hong Kong buying office has used First Sale valuation for over a decade. The difference between the mill price and the buying office price is typically 15-25%. By basing customs value on the mill price, they reduce their duty bill by 15-25%. The administrative burden is significant—they maintain a dedicated compliance team that audits every First Sale transaction—but at their import volume, the savings are in the millions. For more detailed analysis, reading CBP's official guidance on the First Sale for Export valuation method, including the specific legal requirements and the documentation that must be maintained is the regulatory starting point, and understanding the practical implementation challenges and audit risks of First Sale valuation in the textile and apparel industry, with guidance on building a compliant program is essential before pursuing this strategy.

Can the "De Minimis" Threshold Be Used for Fabric Samples?

Yes, and this is a tariff minimization strategy that almost every fabric buyer should be using for their sampling and development phase, but many don't because they simply don't know it exists. The "de minimis" threshold is the value below which imported goods can enter the US duty-free and with minimal customs formalities. In 2026, the de minimis threshold for most goods is $800 per shipment, per person, per day.

This means that if you are a fashion brand developing a new collection, and we ship you a sample package containing 10 meters of fabric, some strike-off swatches, and a color blanket, and the total value of the goods is $350, that shipment can enter the US duty-free under Section 321 (de minimis) entry. You pay zero duties. Zero tariffs. Zero customs processing fees. The shipment clears customs quickly and arrives at your door with no additional charges.

This is a perfectly legal, routine provision of US customs law. It's designed to facilitate low-value shipments and reduce the administrative burden on both CBP and importers. The key is that the $800 threshold applies to the "fair retail value" of the goods in the country of shipment, not the FOB price, not the DDP price. Your supplier should state the value accurately on the commercial invoice.

For a brand that goes through multiple sampling rounds—three lab dip iterations, two strike-off approvals, a pre-production sample yardage order—the cumulative duty savings from using de minimis entry can be hundreds or even thousands of dollars over a development cycle. And it's completely legal. The only risk is "structuring"—deliberately breaking up a single order into multiple smaller shipments to stay under the $800 threshold. This is illegal. If the goods are part of a single commercial transaction, they should be shipped as a single entry. But genuine, separate sample orders that each fall under $800 are entirely eligible for duty-free de minimis entry.

A Los Angeles-based designer I work with receives 3-4 sample shipments from us each season, each valued at $200-$600. She's never paid a cent of duty on her samples. She didn't know about de minimis until I explained it. She assumed all imports were subject to duty. Knowing this rule has saved her thousands of dollars over our relationship. For complete guidance, reading CBP's Section 321 de minimis entry regulations, including the $800 threshold, the types of goods that qualify, and the anti-structuring rules provides the official framework, and understanding how to properly document and declare low-value textile samples for de minimis entry, and how to avoid the common pitfalls that lead to rejection or assessment of duties ensures your samples sail through duty-free.

How Can Raw Material Origin Legally Eliminate a Tariff?

Tariffs are not just about where a fabric is stitched or woven. They are about where the fibers were grown, where they were spun, and where they were transformed. The concept of "substantial transformation" and the specific origin rules that govern textile imports can, in certain cases, eliminate a tariff entirely. This is the most powerful tariff minimization strategy, and it's also the most documentation-intensive.

The US tariff system is fundamentally bilateral. When a fabric is imported from China, the "Made in China" label triggers the standard MFN (Most Favored Nation) duty rate, plus any applicable Section 301 China-specific additional duties. However, if you can demonstrate that the fabric is not, in fact, a product of China for tariff purposes—even if it was woven in China—the Section 301 duties may not apply, and a different, potentially lower, duty rate may be available.

The key is the yarn-forward rule of origin. For most textile products, the country of origin is determined by where the fabric is woven, not where the fiber is grown. This is the standard rule. However, there are exceptions and nuances. If the raw material (the flax fiber) is grown and retted in France, and the fabric is woven in China, the "country of origin" for standard customs marking purposes is China. But for certain trade preference programs, or for the purpose of avoiding Section 301 duties specifically, the origin of the raw material can be the decisive factor.

This is where our European flax supply chain becomes a strategic tariff asset. Our SL-550 fabric uses flax grown in Normandy, France, which is a European Union origin material. Under certain duty drawback or foreign trade zone programs, the non-Chinese content of the fabric can be segregated and treated differently. More importantly, if a US importer can demonstrate that the "essential character" of the fabric is derived from the European flax, and that the Chinese manufacturing processes (spinning, weaving, finishing) do not constitute a "substantial transformation" that overrides the EU origin—a legal argument that requires case-by-case analysis—they may be able to argue for an EU origin for tariff purposes, completely avoiding Section 301 duties.

This is not a simple strategy. It requires a formal CBP ruling request, a detailed submission of manufacturing processes and costs, and a strong legal argument. It's not for a 200-meter trial order. But for a brand importing 50,000 meters a year of a consistent fabric with a high-value, traceable EU raw material, the duty savings from a successful origin ruling can be transformational. A US home textiles brand that uses our European flax linen for a premium bedding line is currently pursuing this ruling with their customs attorney. Their annual duty bill on this fabric line is approximately $120,000. If the ruling is successful, they will eliminate the Section 301 component, saving roughly $75,000 per year. The legal fees for the ruling request are a fraction of the potential savings. For a comprehensive understanding, reading CBP's rules of origin for textile and apparel products, including the concept of "substantial transformation" and the specific origin determination rules for woven fabrics is the legal foundation, and studying the CBP ruling database for precedents where non-Chinese raw material origin has been used to avoid Section 301 duties on textile products, including the legal arguments and evidence that succeeded provides the practical roadmap for anyone considering this advanced strategy.

Does the "Yarn-Forward" Rule Apply to Woven Cotton Linen?

The "yarn-forward" rule is the dominant rule of origin for textiles in US trade agreements and preference programs. Under a yarn-forward rule, the country of origin is the country where the yarn is spun, not where the fiber is grown, and not where the fabric is woven. This rule has a specific and powerful implication for cotton-linen blends that use non-Chinese yarns.

If a US importer sources cotton-linen fabric that is woven in China, but the yarn used to weave that fabric was spun in a country other than China—say, linen yarn spun in Italy, or cotton yarn spun in India—and if the applicable trade program uses a yarn-forward rule, the origin of the fabric may be the country where the yarn was spun, not China. This would mean the fabric is not subject to Section 301 China tariffs.

In our standard production, we spin our yarn in our own spinning mill in China, using European flax fiber. So the standard yarn-forward rule confirms Chinese origin, because the yarn is spun in China. However, for specific, high-volume programs, we have the capability to source externally spun yarn—for example, linen yarn spun by a specialized mill in Italy—and weave the fabric in China. If the weaving in China is considered a "simple assembly" process that does not substantially transform the Italian yarn, the origin of the fabric could be argued to be Italy, not China.

This is a niche, advanced, and complex strategy. It requires a dedicated supply chain setup, a separate production run, and a legal analysis of whether the specific weaving process constitutes a substantial transformation. It's not for every product or every buyer. But for a high-volume, high-value program where the tariff differential is significant, the economics of sourcing non-Chinese yarn can be justified by the duty savings alone.

A European luxury brand that produces a signature cotton-linen trench coat fabric sourced Italian-spun linen yarn for their China-woven fabric, specifically to achieve Italian origin and avoid Section 301 duties on their US imports. The yarn cost was higher, but the duty savings on their US volume more than offset the premium. The product quality was also enhanced by the premium Italian yarn. For detailed technical reading, the WTO Agreement on Rules of Origin and the specific yarn-forward, fabric-forward, and cut-and-sew rules that determine textile origin in different trade agreements provides the international framework, and understanding how CBP applies the yarn-forward rule in practice, including the evidence required to demonstrate non-Chinese yarn origin in a woven fabric is essential for anyone pursuing this path.

Can a Section 321 De Minimis Entry Cover Bulk Fabric?

No. Let me be absolutely clear about this, because I have seen online forums and social media posts suggesting that buyers can import bulk fabric orders duty-free by breaking them into multiple $800 shipments. This is illegal. It is called "structuring," and CBP actively looks for and prosecutes this behavior.

Section 321 de minimis entry is for genuine, low-value shipments. A bulk fabric order—300 meters, 1,000 meters, 5,000 meters—is not a low-value shipment. It is a commercial quantity of goods that was ordered as a single transaction. Deliberately splitting a single 1,000-meter order into ten 100-meter shipments, each invoiced at $799, to avoid paying duties and tariffs, is a violation of 19 USC 1592 (the penalty statute for fraud, gross negligence, and negligence). The penalties include seizure of the goods, a monetary penalty up to the domestic value of the merchandise, and potential criminal prosecution for intentional fraud.

CBP's data analytics systems are specifically designed to detect structuring patterns. They look at the importer's history, the frequency of shipments, the similarity of the goods, and the declared values. If a single importer receives five shipments of the same fabric from the same supplier in one week, each valued at $799, the system will flag this as potential structuring. An investigation may follow.

The de minimis rule is a wonderful, legal tool for sample shipments and small development orders. It is not a tariff avoidance scheme for commercial bulk fabric. Using it as such is not a tariff minimization strategy; it's a criminal act. The distinction is crucial. Use de minimis for your samples. Use the legal tariff minimization strategies—correct HTS classification, First Sale valuation, raw material origin analysis—for your bulk orders. Do not blur the line. For a clear legal line, reading CBP's enforcement guidelines on Section 321 structuring, including the indicators that trigger an investigation and the penalties for violations is essential reading for any importer, and understanding the legal definition of a "single commercial transaction" and how CBP aggregates shipments to determine if structuring has occurred will keep you on the right side of the law.

What Documentation Does CBP Accept as Proof for Zero-Rate Claims?

A zero or reduced tariff claim is only as good as the documentation that supports it. CBP operates on a "show me, don't tell me" basis. If you claim that your fabric is classifiable under a flax heading with a lower duty rate, or that it qualifies for a raw material origin exclusion, you must be able to produce, upon request, clear, convincing, and verifiable evidence. A generic, one-page "mill certificate" with a stamp is no longer sufficient. In the 2026 enforcement environment, CBP expects a comprehensive, auditable documentation package that traces the product from the raw fiber to the finished fabric.

The foundation of this package is the Fiber Composition Test Report from an ISO 17025-accredited laboratory. This is a chemical dissolution test (usually to ISO 1833 or AATCC 20A) that quantitatively determines the exact percentage of each fiber type in the fabric. The test report must identify the specific fabric lot or shipment, and it must be dated within the last 12 months. A report that says "55% Flax, 45% Cotton, ±2%" is the objective, scientific proof that your HTS classification under the flax heading is correct.

The second essential document is the Mill Certification Letter. This is a detailed, signed letter on the manufacturer's letterhead that states: the full legal name and address of the manufacturing facility, the exact fiber composition of the fabric, the country of origin of each fiber (e.g., "Flax fiber grown and retted in Normandy, France. BCI Cotton fiber grown in Maharashtra, India."), the country where the yarn was spun, the country where the fabric was woven and finished, and the applicable HTS code. The letter should reference the specific proforma invoice and packing list for the shipment.

The third document, for claims related to raw material origin, is the Raw Material Purchase Records and Traceability Data. This is where the blockchain-based Digital Cotton Passport we provide at Shanghai Fumao becomes invaluable. The Passport links the specific fabric lot to the specific bales of European flax, with purchase invoices from the scutching mill, transport documents, and GPS coordinates of the farm cooperative. This is the "clear and convincing evidence" that CBP requires to accept that the flax content is genuinely of European origin.

A US importer who received a CBP Request for Information (CBP Form 28) on their SL-550 entry in early 2026 provided this exact documentation package. The fiber composition test confirmed the 55/45 ratio. The Mill Certification detailed the French flax origin. The Digital Cotton Passport provided the farm-to-fabric traceability. CBP accepted the classification and the origin claim and closed the inquiry with no duties assessed. The importer's preparation paid off in a stress-free audit outcome. For a complete checklist, reading CBP's "Reasonable Care" compliance checklist for textile importers, detailing the specific documents and verifications expected for classification, valuation, and origin claims is the official guide, and understanding how to build and maintain a comprehensive, audit-ready customs compliance file for each imported textile product, including record retention requirements and best practices for document management prepares you for the audit that will eventually come.

How Do I Prove the Flax in My Linen Is European and Not Chinese?

Proving the origin of a natural fiber is a forensic exercise. You cannot simply state "Flax: France" on a certificate and expect CBP to accept it. The claim must be backed by a chain of evidence that links the specific fabric to the specific agricultural source. This is where the difference between a generic supplier and a traceable one becomes commercially and legally decisive.

The evidence chain begins at the farm. The flax cooperative or the scutching mill (where the flax stalks are processed into fibers) must provide a certificate of origin for the raw flax fiber. In France, this is often issued by the local Chamber of Agriculture or by the European Flax and Hemp Confederation (CELC). The certificate states the harvest year, the region of cultivation (e.g., Normandy, Flanders), and the quantity of flax fiber produced.

The next link is the spinner. The spinning mill that converts the flax fiber into yarn must maintain batch traceability records. When we receive a shipment of French flax fiber, it is assigned a unique batch number. This batch number follows the fiber through the spinning process and is linked to the specific cones of linen yarn produced. Our spinning records show: "Batch F-2026-03, French Normandy Flax, received January 2026, spun into Nm 28/1 linen yarn, Lot LY-2026-078."

The final link is the weaver. The weaving mill records which yarn lots were used to produce which fabric lots. Our weaving records show: "Fabric Lot SL-550-2026-0421, warp yarn Lot LY-2026-078, weft yarn Lot CY-2026-089 (BCI Cotton)."

When these records are combined—farm certificate, spinning batch records, weaving lot records—they form an unbroken chain of custody. The Digital Cotton Passport consolidates these records into a single, verifiable digital document with a blockchain-anchored audit trail. This is the level of evidence that satisfies CBP's origin verification requirements. A vague "Flax: Europe" statement without this chain of evidence is insufficient and will be rejected. For more on this, reading about the European Flax certification and traceability system, including how the CELC certifies the origin of premium European flax fiber is the industry source, and understanding CBP's evidentiary standards for natural fiber origin claims in textile imports, and the specific types of documents that are accepted as proof of agricultural origin provides the enforcement perspective.

Is a "Handshake Deal" on Tariff Payments Legally Binding on CBP?

No. A handshake deal, a verbal agreement, a friendly email, or a "don't worry, we'll handle it" from your supplier has zero legal weight with US Customs and Border Protection. CBP's legal relationship is with the importer of record. If the importer of record is you, you are legally liable for the accurate classification, valuation, and duty payment, regardless of what any other party promised.

This is a critical point that many first-time importers misunderstand. If your supplier tells you, "Don't worry about the tariff, we'll mark it as a gift," or "We'll put a lower value on the invoice, that's what everyone does," they are asking you to participate in customs fraud. They will not be the ones facing the penalty. You will. The supplier is in China. CBP's enforcement jurisdiction over them is limited. CBP's enforcement jurisdiction over you, the US importer of record, is absolute.

The only thing that is legally binding on CBP is a formal, written ruling issued by CBP itself, or a documented, legally sound customs entry supported by the evidence I've described. If you want certainty on a tariff classification or an origin claim, you can request a binding ruling from CBP. This is a formal legal process where you submit your product details, your proposed classification, and your legal argument, and CBP issues a written decision that is binding on all US ports of entry. A ruling takes time (typically 30-90 days) and often requires legal assistance, but it provides absolute certainty.

Short of a binding ruling, you must rely on your own documented due diligence. Keep the fiber composition test reports. Keep the mill certifications. Keep the origin traceability records. If CBP audits your entry, you will be judged on the documentary evidence you can produce, not on what your supplier told you in a WhatsApp message.

I tell every new client: don't take my word on the tariff classification. Verify it with your own customs broker. We provide the documentation; your broker provides the independent verification. That's the system. That's how you stay compliant. For complete guidance, reading about the CBP binding ruling process, including how to submit a ruling request, the information required, and the legal effect of a ruling on future imports is the official procedure, and understanding the legal liabilities of the importer of record under US customs law, and why verbal assurances from a foreign supplier provide no legal defense in a customs enforcement action should be required reading for anyone importing goods.

Conclusion

You cannot "avoid" US tariffs on Chinese fabric imports in 2026 by hiding, evading, or hoping. The enforcement environment is too sophisticated, the penalties are too severe, and the risk is existential for your business. But you can legally, ethically, and significantly minimize your tariff burden by mastering the system that assesses those tariffs. The HTS code is a decision, and a correct classification under the flax heading instead of the cotton heading can save you 4-5% on the base duty alone. The raw material origin of your fabric is a potential exemption from Section 301 duties, if the fiber is European flax and the documentation is rigorous. The First Sale for Export rule can reduce the customs value, and therefore the duty, if your supply chain has an earlier transaction that qualifies. And for samples and small development orders, the $800 de minimis threshold is a legal, routine, duty-free pathway that every brand should be using.

The common thread through every one of these strategies is documentation. At Shanghai Fumao, we invest in traceability, in testing, in the Digital Cotton Passport, and in the precise specification of every raw material, not because it's a marketing advantage, but because it is the legal foundation upon which legitimate tariff minimization is built. A supplier who gives you a "good price" but can't give you a fiber composition test report, a mill certification, and a traceable origin record is a supplier who is exposing you to a customs liability you can't afford.

If you're importing fabric and want to ensure your tariff strategy is optimized, compliant, and audit-proof, start by sourcing from a supplier that provides the documentation package CBP requires. To discuss your specific fabric, your HTS classification, and the tariff minimization strategies applicable to your supply chain, contact our Business Director, Elaine. She can provide the full compliance documentation for any of our fabrics, and she can connect you with the US customs brokers we work with who understand textile classification and origin. Her email is elaine@fumaoclothing.com. Don't try to avoid the tariff. Learn to master it, legally.